Data is the life-blood of an insurance company

The insurance industry is a data engine: insurance firms create data, capture external data, process data, and output data. Stripping away the various processes of an insurance company (looking beneath the layers of processes as if an x-ray was taken of a human body), we would find that data flows within, among, and throughout an insurance company and the value web that envelopes the insurance company.

Data is the life-blood of an insurance company.

This reality is why data analysis has always been an integral part of the insurance strategy practices’ research agendas I have led. Before becoming an industry analyst, data analysis was an integral part of my life during my almost 20 years working in the marketing / market research departments of the insurance industry.

What I consider to be part of data analysis

But what do I consider to be part of ‘data analysis?’

For me, ‘data analysis’ spans ‘digits to documents.’ That is why semantic analytics and text data mining have always been included. Also included is data analysis focused on ‘where’ because the topic of location is critically important to the insurance industry (pick your favorite insurance line of business). Location encompasses Geographic Information Systems (GIS), geospatial, location intelligence, and, more recently, earth observation / NewSpace.

The above paragraph is rather short but encompasses an extensive set of data analysis topics, issues, and questions that can drive major areas of research, reporting, and presenting for any insurance industry analyst.

For the purpose of this post, I want to discuss how any one of the data analysis topics alone or in some combination can answer the questions associated with the five levels of data analysis.

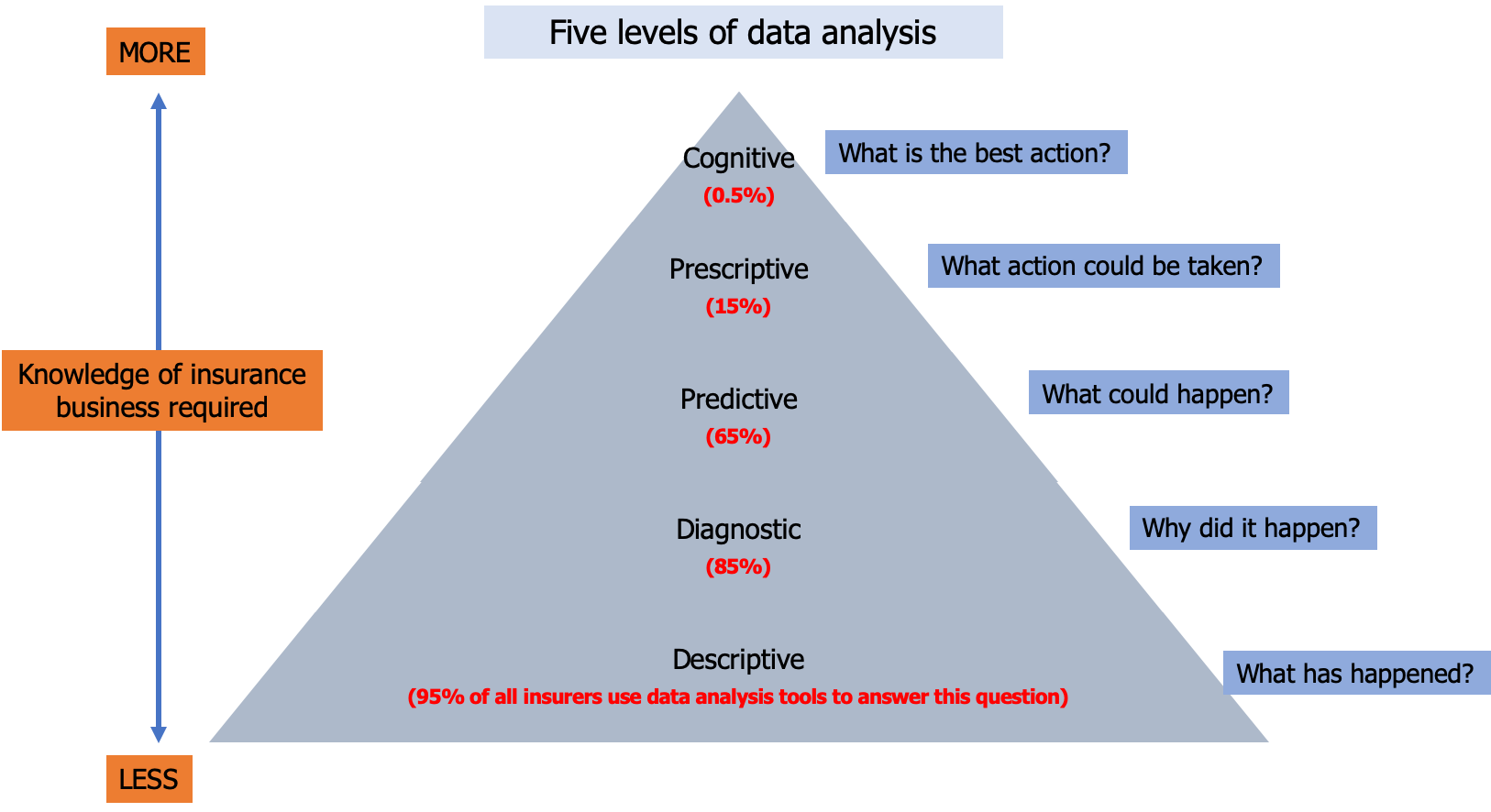

Five levels of data analysis

I believe that most of us, if not all of us, have seen a diagram, such as the one below, of different types of data analysis that captures questions about the past time-frame, the current time-frame, and a potential future time-frame.

The diagram also implicitly captures the increasing level of knowledge of the business, company resources (current and future), company tactics, and company strategy that is needed to answers the questions as the time-frame moves from the past to the current to the future.

The past-driven questions

In the beginning of my insurance career (right after the dinosaurs disappeared from the planet), we focused almost entirely on the first two data analysis past-driven questions: what has happened and why did it happen. Cross-tabulations and time-series were the primary data analysis tools we relied on most of the time.

The future-driven questions

At some point during the subsequent decades, the two future-driven questions were added to the ‘should be answered’ list: what could happen and what action could be taken. More than cross-tabulations and time-series were definitely required. More serious predictive modeling came to the fore. Artificial Intelligence (AI), and its own expanding set of capabilities, became a growing part of the data analysis tool-set.

Of course, the ‘what action to be taken’ answer required knowledge of the business issues, tactics, and even company strategy. One problem that I remember was our company not having a coherent strategy (although it may have had a strategy and I just didn’t remember it at the time).

The cognitive question (yes, it is a future-driven question)

Finally, the question of determining the best action has been (recently – a subjective term I realize) added to the list completing a robust spectrum of questions that should each be addressed for business issues throughout the insurance value web of getting-and-keeping clients.

Answering the question decidedly requires more than data analysis tools such as neural nets, machine learning or deep learning: it also requires significantly more knowledge of the business, its current and potential resources, tactics, and strategy. (Assuming the insurance company has a strategy – preferably coherent and known throughout the company.)

What is your insurance company doing?

I’m sure that you won’t be shocked to learn that I believe that extremely few insurers are answering the ‘what is the best action’ question by using AI data analysis tools or, for that matter, any data analysis tools. We are flooded with technology firm’s news releases, press releases, or surveys about the applications of their newest AI-shaped data analysis tools. It is difficult to not see Data Scientists, AI, machine learning, deep learning, and even an occasional Neural Net mentioned frequently in the insurance trade press.

All that digital ink aside, I don’t believe insurers are moving that quickly up the triangle.

A higher percent of large insurers may be using data analysis tools to answer all five questions. But smaller and mid-size insurers? I don’t believe that they are using data analysis tools in any ‘reasonable’ numbers: they aren’t moving the needle, so to speak, that measures the total % of insurers using data analysis tools to answer questions 3, 4, and 5.

I would have to see the results of an objective and statistical-based survey of the insurance industry, preferably by line of business, to believe it.

My wild guess

My wild guess, considering the entire insurance industry, would be these %’s of insurers using data analysis tools to answer each of the questions:

I hope I’m wrong. I’m probably low (very low?) about the %s of all insurers using data analysis tools to answer the two questions at the base of the triangle. But I’m probably guessing too high about the 0.5% of all insurers using cognitive data tools to answer the ‘what is the best action’ question: a question that encompasses both strategic interests nt and tactical initiatives needed to realize the strategic vision.

What do you think are the %s of (all) insurers using data analysis tools at each level? How do you it differs by major line of insurance business?

Barry- what of the thought of where the opportunities are for AI as a service lay, say predictive and prescriptive? Take for example fraud detection applications. Might be more cost effective for a vendor to leverage a carrier’s descriptive and diagnostic analysis in applying the vendor’s proprietary tools using levels three and four.

As for Cognitive- might remain an analog/digital balance.

LikeLike

I think you have the breakdown just about right – Cognitive at 0.5% may be a reach but not so far off. If you break it down by size of company as measured by GWP I think you will find that companies outside of the top 10 are not close to those benchmarks unless they are reinsuring most of their business and it is driven by the reinsurer. Same applies by line of business – while I think P&C has made some headway and Health is trying to move that way, Life is standing still.

LikeLike