(Before going any further in this post, I want to state that I firmly believe that insurance, pick your favorite insurance line of business, is not a commodity. I do not intend my discussion of differentiation to imply or assert otherwise.)

————————————————————-

Do insurers differentiate themselves from each other in the minds of their customers? Do insurers have a recognizable brand that resonates with customers as offering unique value from other insurers? Do insurers exist that have points of differentiation and/or brand (again, in the minds of their customers) that enables them to take customers – and profitable revenue – away from other insurers? (Well, other than USAA and AMICA with their continual high ratings for customer service.)

The insurance industry is (very obviously) an extremely mature industry (as well as a very large and heavily regulated industry). Is it necessary for insurers to have points of differentiation and/or a brand that implicitly delivers a compelling unique value proposition in a mature – and slow to change – industry?

Boiling the above paragraphs down into two questions:

- Do insurers differentiate themselves from each other in the minds of the customers?

- Do insurers need to differentiate themselves from each other in the minds of the customers?

Tackling the two questions

To tackle the first question, I’m going to use Geoffrey Moore’s description of core and context from his book “Dealing With Darwin: How Great Companies Innovate At Every Phase of Their Evolution” as the foundation of my discussion.

Core and Context

In this book, Geoffrey Moore defines these two terms (direct text from multiple parts of his book) in this manner:

- Core: Any aspect of a company’s operations that creates differentiation of your company to create sustainable competitive advantage leading to customer preference during a purchase decision.

- Context: Everything else, all other work performed by the enterprise, including most of the activities the company does to meet the commitments to key stakeholders – investors, employees, customers, and partners – and to comply with the laws of your nation and the standards of your industry. It also includes all the activities the company does to keep pace with its competitors and meet what has become the market’s standard of performance.

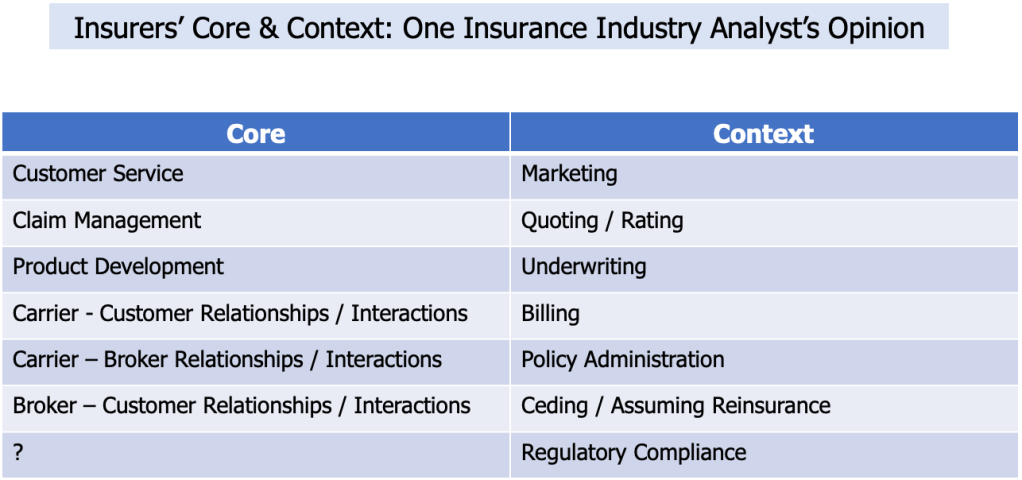

In the table, I suggest some insurance activities that are “core” and some that are “context.”

(Im sure that you realize from the table that I am separating “customer service” from other aspects of policy administration.)

Having worked for several insurers during the first 17 years of what would be a four plus-decade insurance career, I know that every insurer that employed me believed that they offered a unique value proposition to their customers and would put one or more of their activities in the “core” category. I rarely believed the insurers I worked for (other than AEtna Life & Casualty who I considered, at that time, to offer claim management as a sustainable competitive advantage back in the 1970s-1980s).

When I became an insurance management consultant in the late 1980’s with Arthur D. Little (and in subsequent years worked for IBM Global Services and BearingPoint), I’d often ask insurance clients during strategy engagements “what is your value-add?” I’d ask them not to reply ‘billing” or “underwriting” or “policy administration.” That left several of them staring at me with a blank expression because I had removed some of their options.

I am not stating that an insurer couldn’t transform any of the “context” activities into “core” activities. Remember though that the impact has to be felt by the insurer’s customers (and not by the management or employees of the insurer or by the agents or brokers the insurer uses to reach and serve its customers).

Similarly, I am not stating that any of the “core” activities couldn’t be viewed as “context” from the perspectives of an insurer’s customers or, in actuality, aren’t “context” activities.

Insurers with “core” activities

I imagine there are many cynics who would state that every activity I have listed as “core” are actually “context.” And further, that all (most?) insurers don’t do anything to create differentiation in their customers’ minds.

But, from my perspective having worked in, consulted to, and been an analyst of the insurance industry all totaling 40+ years, there are insurers who create sustainable competitive advantage through some of the “core” activities I have listed in the table.

I always use USAA and AMICA as examples in the personal P&C insurance industry marketplace as prime examples of insurers creating (and maintaining) a sustainable competitive advantage in customer service and claim management. I’d place Chubb in the product development “core” category as well as the customer service “core category” based on what I’ve heard from Chubb customers.

Goodness knows that leaves many other insurers (thousands, actually) in the personal P&C insurance industry marketplace as well as insurers in the commercial P&C insurance and individual Life & Annuity insurance industry to think about as being mostly “context” – laden or all “context”-laden.

I’m sure you have noted that all of the “core” activities, other than product development, involve customer interactions. More than that, the activities involve the ability to relate to customers, to have empathy with, and to offer customers infinitely more than a text, email, IM, or mobile app can ever hope to provide.

Over to you: what other insurers in the personal P&C insurance, and/or commercial P&C insurance, and/or individual L&A insurance industry come to mind as having activities you would categorize as “core?” Which activities of each of those insurers are you thinking about as “core”?

Do insurers need to have points of differentiation?

My second question is: do insurers need to differentiate themselves in the minds of their customers?

My answer is an absolute ‘yes!’

But this post is long enough.

I’ll get into my rationale of why my answer is ‘yes!’ in a subsequent post.