Note 1: This (very long) post is an excerpt from a research report of the same title that I co-authored with Christopher Frankland in June 2018

Note 2: When you read this post, mentally replace every instance of “Virtual Assistants”, “Assistants”, “External Assistants”, and “Internal Assistants” with Gen AI or Agentic AI. Then, consider what guardrail procedures are required to ensure that the AI technology applications provide correct information throughout the communications.

Commerce requires a bridge connecting customer acquisition and retention

Insurance commerce is composed of two interdependent initiatives: customer acquisition and customer retention. Insurance firms have primarily relied on two separate and distinct sets of systems (by systems we include technology, processes, information, and people) to acquire and retain customers. Insurers’ customer acquisition systems include agency management; customer relationship management; pricing, rating, and quoting; underwriting; product development; and marketing and sales. Insurers’ customer retention systems include core administration, fraud management, and financial management.

The reliance on siloed systems to get and keep customers is no longer viable, assuming it ever was. Competitive success of insurance commerce, specifically in our mobile digital interconnected marketplace, mandates that customer acquisition and retention systems quickly become interdependent.

Virtual Assistants (VAs) – whether text-based IM or voice-responsive bots – are a bridge that simultaneously enables and requires data to easily and quickly flow between an insurance firm’s customer acquisition and retention systems. As importantly, the effort that insurers invest in planning for, deploying, and using VAs helps to create a permanent mindset to continually identify and support the interaction needs of clients to conduct commerce.

Simply stated, VAs are a mechanism that forces insurance firms to think and operate from an outside-in customer orientation rather than thinking and operating from the traditional inside-out insurance firm orientation.

Commerce is a VA-ready web of customer-centric communications

Insurance commerce creates a bridge for the data flowing between customer-facing and core administration systems. These data flows provide a ready web to support VA-driven insurance commerce. The customer-centric communications encompass information, questions, application forms, and policy documents moving between and among many participants involved with the purchase of insurance.

Insurance participants include the insurance agency’s producers, CSRs, and administrators involved with the sales and servicing of the customer; and at times, the insurance company’s CSRs, underwriters, and sales and distribution professionals. During loss events, other participants are also involved in retaining insurance customers, including third-parties such as claims adjusters, healthcare providers, and property remediation and restoration specialists.

The data-intensive communication flows, represented as tangible and intangible artifacts, travel over terrestrially-based geographies and/or stream through digital strands connecting the participants. The tangible artifacts encompass hard-copy facsimiles, forms, and documents and the intangible artifacts encompass telephony communications, instant messaging, emails and other electronic or digital interactions.

Conducting insurance commerce using a customer perspective – the outside-in perspective – is the primary component of competitive success. This is particularly true for insurers who realize that commerce is a web of communications between customers and insurance professionals that provides the content – and context – enabling the successful deployment of VAs.

Query resolution highlights customer frustration factors

Insurance customer service includes frustration factors in resolving queries

Insurance firms have an opportunity to use VAs to minimize some (most?) of the frustration that develops when customers interact with the insurance firm, insurance agency, third-party claim adjuster, or others involved with the customer’s query.

There are many sources which seem annoyingly integral to an insurance company’s customer service process that contribute to a customer’s frustration, including customers having to:

- navigate through the insurer’s VRU tree and hope, at a minimum, the options the customer expects are included in the panoply of choices

- wait for the CSRs and/or other professionals tell them that they can resolve the customer’s issue but have to take time to retrieve the requisite information from sources not immediately available to them.

- repeat themselves several times:

- during one interaction with the VRU and/or CSRs or other home office and/or agency professionals

- throughout multiple interactions with two or more CSRs or other home office and/or agency professionals even if a VRU isn’t used during the interactions.

Customers needing their own resources generates frustration to resolve queries

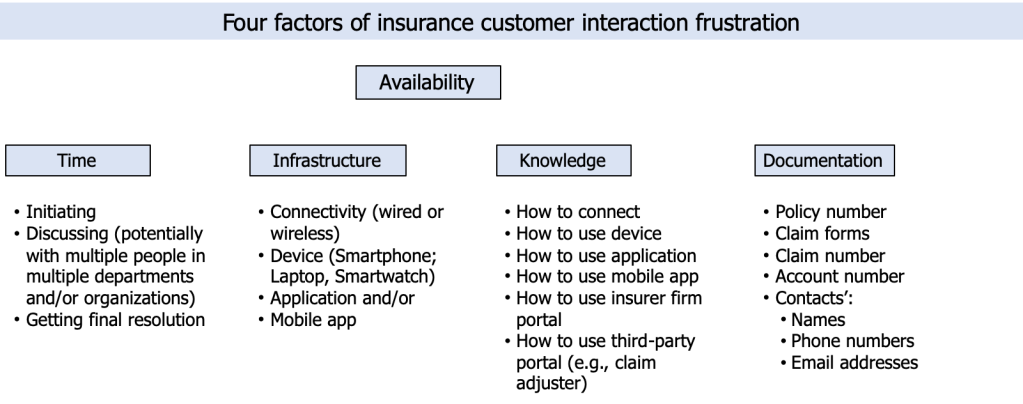

The insurance firm is (quite obviously) not the only participant in the insurance commerce interaction using its own resources to fulfill a customer issue. The resources which a customer uses to initiate and resolve a request include time, infrastructure, knowledge, and documentation. Each of these four resources encompasses a set of actions, devices, apps, learned experiences, and accessible paperwork and/or digital files.

Moreover, needing to have any or all of these four resources available at all or in part can be factors that contribute to customer interaction frustration. (See Figure of four factors of insurance customer interaction frustration.)

Insurance companies too often forget or completely ignore the resources customers have to, or think they need to, have available before they initiate a request, or worse during the conversation, about an issue or question they need resolved.

The reality of a customer-insurer conversation: there is only one conversation

We realize this may just be a hypothesis but we submit that customers don’t want to interact with multiple insurance professionals at all or merely one insurance professional multiple times to get a resolution of their question. Whether the customer has to interact with an insurance firm (or insurance agency or claim adjudication firm) more than one distinct time or talk to multiple people (in any of those firms) multiple times to resolve their query, the customer believes that the totality of all of these interactions is only one conversation.

Insurance firms which deploy VAs won’t necessarily reduce the totality of interactions the customer has to endure to only one interaction. However, we believe that understanding the dynamics of a conversation using a framework of a meta perspective of requests and responses will assist insurance firms determine how and where to deploy VAs to resolve issues more effectively and more efficiently.

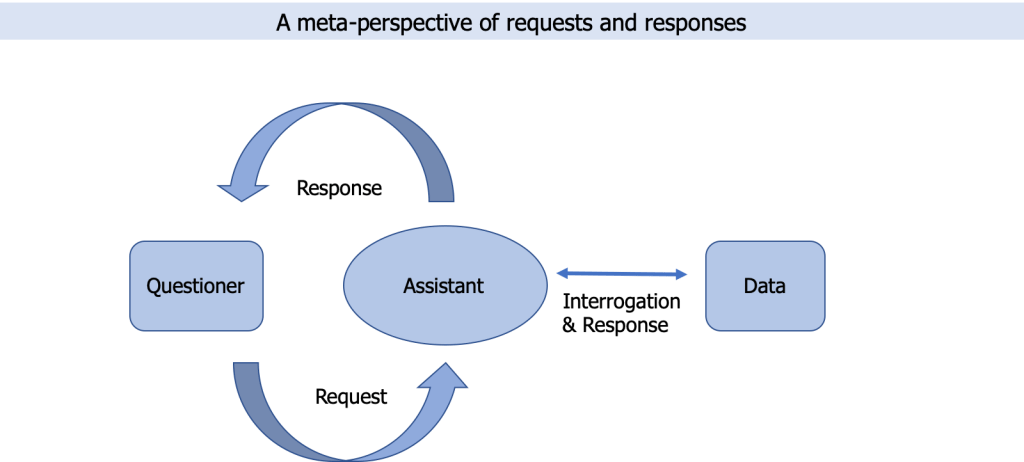

A meta-perspective of requests and responses between Questioners and Assistants

Creating a path to fulfill the customer’s query quickly and minimizing insurance customer frustration requires insurers to reconsider the conversation of request and response from a meta perspective. (See Figure of a meta-perspective of requests and responses.)

Note: there is a blog post or sequence of posts that cry out to be written about the “data” aspects of this meta-perspective. What is the availability of the data? What is the accessibility of the data? How ‘clean’ is the data? Is the data accessed the ‘one-and-true’ data without any variants anywhere (even in desk drawers or departmental file cabinets)? Does everyone agree on the exact same definition of the data? These questions concerning ‘data’ only scratch the surface, if that, about the questions that need to be resolved before the ‘data’ can be used in a communication between customers and insurance firms / agencies / claim adjudicators / ….

The meta perspective reveals key functions and resources that comprise the essence of the customer-insurance firm conversation:

- Questioner who initiates the query could be:

- an insurance customer

- one or more producers or others in an insurance agency

- one or more people from a third-party contractor to the insurance firm (i.e. a claims adjuster)

- one or more professionals in an insurance company

- a VRU used one or more times during the processes of fulfilling the Questioner’s request

- one or more VAs used by any of the (human or other VA) entities.

- The Questioner’s Request could come into the insurance firm from a customer’s telephone call, email, IM, use of social media, use of company portal, or VA (whether smart speaker or mobile app).

- Assistant responding to the Questioner’s request could be:

- one or more CSRs or other professionals from the billing, underwriting, claims, or other departments in the insurance company

- one or more CSRs from an insurance agency

- one or more producers from an insurance agency

- one or more CSRs from the third-party contractor claim adjuster firm

- a VRU used one or more times during the process of fulfilling the Questioner’s request

- one or more VAs used by any of the professionals, or other VAs, tasked with interacting with the Questioner in any of the above companies.

- One or more sets of data available in a form that is needed to interrogate and fashion a response to the Questioner.

- The conduits of commerce and information (C&I) available to the customer to connect with the insurance firm to register a request and to receive a response.

- The availability of tools to the Assistant to access, interrogate, and create a response to answer the Questioner’s request.

- The Assistant’s Response could be delivered to the Questioner in the form of a vocal answer; an IM, email, telephone call, or written letter; or entry into Questioner’s financial management system (i.e. Quicken) or bank checking / savings account.

The meta perspective reinforces that Questioners or Assistants enabling or supporting the insurance commerce processes could be people (insurance agents, brokers, MGAs, or MGUs, CSRs, claim personnel), telephonic systems (i.e. VRU), or software solutions (i.e. VA), or any combination of these involved in the purchase -and service – of an insurance policy.

Four directional flows of requests and responses

Insurance firms, whether carriers or agencies, may decide to initially deploy VA solutions to support requests from their current or prospective policyholders to transform the implicit promise of VA solutions into an explicit reality. However, that is a myopic perspective of planning where to implement VA solutions to enable insurance commerce.

We view insurance commerce as the entirety of the processes to get and keep customers, including product development, marketing, sales and distribution, service, and claims management.

To support the holistic view of insurance commerce, insurance firms should consider four directional flows of requests and responses for VA deployment. (See Figure below of directional flows.) The four directional flows encompass the conversation between the locus of Questioners and the locus of responses. The Questioners could be external customers or internal customers. Similarly, the responses could be from external assistants or internal assistants.

Description of “customer”, “external”, and “internal” terms in the figure of direction flows

Before discussing examples of each directional flow, consider our description of ‘customer’, ‘external’ and ‘internal’ terms in the above figure.

We use the term ‘customer’ to encompass more possibilities than an existing or prospective policyholder person requesting service. A ‘customer’ is any person, or VA used by a person, connecting with or within a firm participating in the insurance value chain with a request to:

- for information to answer a query (learn)

- to request forms or documents (receive)

- to determine the status of an activity within a process (track)

- to initiate and/or fulfill a monetary transaction (do).

We use the term ‘external’ to refer to any person, whether Questioner or Assistant, who does not work for insurer, insurance agency, third party claim adjuster, or other firm involved in the insurance value chain.

Contrariwise, we use the term ‘internal’ to refer to any person, Questioner or Assistant, who does work for the insurer or within an insurance agency, third party claim adjuster, or other firm involved in the insurance value chain.

Examples of the directional flows

Using the above discussion defining terms as context for the deceptively simple appearing Figure of directional flows, consider the directional flows with some examples are:

- An external customer connects with an external Assistant with a question or receives information from the Assistant (note the direction of the two arrows in the box in the top left of the figure): This path encompasses a policyholder requiring a response from their family members, law firm or medical provider. This path also encompasses policyholders receiving information from their family members, law firm, or medical provider.

- An external customer connects with an internal Assistant with a question: This is the current path being used by insurance firms to deploy VA solutions.

- An internal customer connects with an external Assistant with a question: This path encompasses professionals working within an insurance firm (i.e. insurance carrier, insurance agency) requiring a response from an automobile repair shop, a property remediation firm, or a medical provider.

- An internal customer connects with an internal Assistant with a question or receiving important information from an internal Assistant (note the direction of two arrows in the box in the bottom right of the figure): This path encompasses one or more insurance professionals requiring a response from:

- Colleagues in the same department of the same insurance firm. Note that the March 30, 2018 Wall Street Journal reported that Allstate is using “an AI-powered chatbot called Amelia which is designed to help Allstate employees solve customer inquiries faster and more efficiently by answering questions via an instant message platform on their desktops.”

- Colleagues in different departments of the same insurance firm

- Colleagues from different firms within the insurance value chain (i.e. from a third-party claim adjuster firm, from a sub-contracted outside law office, from a reinsurance firm)

This path also encompasses one or more insurance professionals receiving information from company management (i.e. merger or acquisition information, change of management structure), department heads (i.e. updated underwriting requirements, alerts about new products), or their department colleagues (i.e. new procedures).

Concluding remarks

We don’t think it is a stretch to state society is quickly entering an era of AI-driven virtual assistants (VAs) being available to inform, entertain, and help customers transact commerce with a growing portfolio of businesses.

Three non-trivial questions quickly emerge for insurers to answer who want to use VAs to support commerce:

- What types of VAs do customers expect from their insurance brokers, carriers, claim managers, or other participants offering insurance services?

- Where along the customer journey / insurance value chain should insurance firms deploy VAs to meet, or reshape, customer expectations?

- How should insurance participants prepare to deploy VAs?

The answers that insurers provide to the above three questions and related questions will build a foundation for insurers to use VAs to support insurance commerce.