Media Streaming Services Are Hot !

Now that’s an understatement!

We all know and all are experiencing the continuing ‘hotness’ of consumer media subscription-based streaming services. Netflix already has competition from Amazon Prime and HULU but got more competition when Disney + and Apple + jumped into the streaming party in November 2019 in the US. Next year, AT&T is launching HBO Max and NBCUniversal is launching Peacock to join the fray.

Streaming, or more specifically subscription-based media streaming (to include Spotify and Apple Music) informs consumer expectations about on-demand entertainment. (See visual below.)

More generally, subscription-based streaming services implicitly informs consumer expectations regarding their interactions with other content (and the companies that offer the content) that plays (sorry about that … no pun intended) a critical role in their lives.

Subscription-based streaming services have played a critical role for decades

Beyond subscription-based media streaming services, consumers have been using subscription-based streaming services for many decades.

I’d submit that we have lived in a subscription-based economy for quite some years (particularly with the introduction of credit and credit cards many decades ago). You could probably make a reasonable case that Christmas Clubs that banks created many years ago were a form of a subscription-based streaming service.

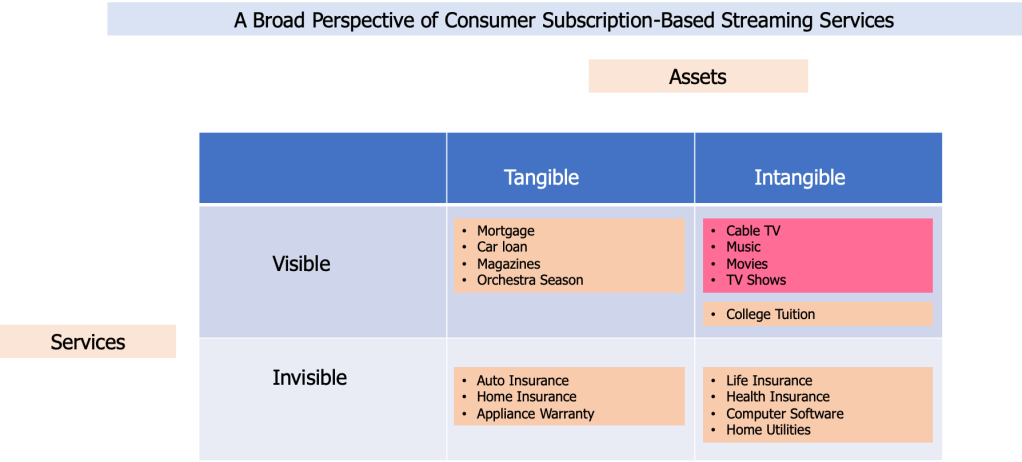

An important point to me is that if a person is paying for a service on a periodic basis (weekly / monthly / semi-annually / annually) than the person is ‘subscribing’ to the streaming service. A second important point is the nature of the services (whether visible or invisible) and the nature of the assets (tangible or intangible) the consumer is paying for in the subscription.

A heuristic that provides a lens into this situation is a visual that captures assets (tangible assets, intangible assets) and services (visible services and invisible services). This framework – with some examples – captures a broad perspective of consumer subscription-based streaming services. (See visual below.)

Tangible and intangible assets

Tangible assets are assets that a person can touch; intangible assets exist but can’t be touched. You’ll note that I added ‘college tuition’ as an Intangible Asset and put it in the ‘Intangible Assets / Visible Services’ box.

Visible and invisible services

Visible services represent services that a person can see or hear (or can live in such as house or apartment that is paid for through time by a mortgage or rent payment). Invisible services encompass auto insurance, home insurance, appliance warranties, computer software, and home utilities as examples.

Categorizing insurance is a mixed bag depending on line of business

I divide insurance between tangible or intangible assets. Auto insurance and home insurance are tangible assets (you can touch and see your car or home) supported by invisible services. (I realize you can ‘feel’ poor service but that doesn’t make it ‘visible’ in the sense I mean.) Life insurance and health insurance are both intangible assets supported by invisible services.

The intangible asset in the case of life insurance is the provision to the policy beneficiary of a cash payout or an income stream.

Implications for the insurance industry

The obvious implication is that insurance offers an invisible service regardless of line of business.

And another obvious implication is that the insurance industry is in the “provide peace-of-mind to customers by paying their claims” business. Of course, the only claims, or parts of claims, that insurers should pay are those claims (or parts of claims) that meet the terms, conditions, and restrictions of the insurance policy.

But there is yet another implication for the insurance industry and it rests on the first implication of insurance companies providing an invisible service.

Customers can’t see that they are protected by their insurance policy every day, every week, every month, and every year during a time period in which they keep their insurance policies in-force. This situation constantly begs the question in the insurance customers’ minds of “what am I paying for?” They can’t see the constant protection (until time of claim) and so their always-present protection is not continually reinforced in their minds.

Insurance represents a subscription-based streaming service that offers a blank screen in the minds of too many insurance customers. This reinforces the old insurance industry quip that “we’re in the premium collection business … not the claim payment business”.

What should insurers do to reinforce the continual (invisible) service for their customers?

A dash of reality

A few facts come into play to shape the reality of what insurance firms (carriers; agencies / broker firms) can do:

- Insurance firms are not legally allowed to rebate premiums (or I assume take any action that an insurance regulator perceives as the equivalent of a rebate)

- Insurance agents/brokers are not legally allowed to rebate commissions (or I assume take any action that an insurance regulator perceives as the equivalent of a rebate)

- There will always exist a per cent of insurance customers who understand they are continually protected by their insurance policy as long as they keep the insurance in-force (including having a paid-up life insurance policy).

Insurers can make the ‘invisible’ visible

Having spent so many decades working in and around the insurance industry (and being an insurance customer) I realize that agents often send calendars and birthday cards, anniversary cards, and other greetings cards to their customers. These tokens never meant much to me personally. Maybe they mean more to other insurance customers.

What then beyond these tokens? Is it legal for an insurance company or an insurance agency / broker firm to invite customers to local events in or around where they live or work? Perhaps provide free or discounted tickets to live music events? Or sports events?

I’d suggest that insurers can make the ‘invisible’ visible by enabling insurance customers to be able to access their own insurance information whenever they wanted, including:

- providing a private, secured “vault” to put the customer’s insurance policies, pictures and when applicable to the customer’s types of insurance policies – videos of the customer’s home and contents, pictures and videos of customer’s claim events

- current report (updated weekly or more frequently when required triggered by any changes to the detailed information on the report as shown in the bullets below) personalized for the customer encompassing the policy / policies the customer continues to have in-force as well as news about and updates to the insurance company’s and/or insurance agency/broker firm mobile apps

- dates: of each policy purchased, of in-force time period, of next premium due, of terminated or lapsed policies

- copies of each of the currently in-force insurance policies

- name and address of the insurance agency / broker firm of the selling and/or servicing agent or broker

- name, telephone number, email, and business addresses of the customer’s agent-of-record unless the agent has left the insurance agency / broker firm … but then provide the name, telephone number, email, and business address of the customer’s servicing agent

- for individual life insurance and/or annuities:

- cash value information (current and historical)

- loan information (current and historical)

- time-line of yields for equity-linked life insurance policies and/or annuities

- dividend (current and historical) information for participating life insurance policies (yes, I know that the ‘dividend’ in this case is a return of premium due to actuarial assumptions for the year that were too conservative)

- premium information (current and historical)

- for personal lines property/casualty:

- record of customer service interactions, time and date the customer reached out for customer service, customer’s reason for reaching out for service, names of service representatives involved with customer service request, status of resolution of customer’s service request, amount of time (minutes, days, weeks, …) it took the insurer to resolve the service request to the satisfaction of the customer

- record of claims including time and date of each claim; nature of each claim; pictures / diagrams of each claim, names, telephone numbers, and emails of every person involved with the adjudication of each claim (including third party claim adjusters, rehabilitation firms and their staff involved with each of the customer’s claims; restoration firms and their staff involved with each of the customer’s claims), time to resolve the claim to the customer’s satisfaction (days, weeks, months, years); and the amount the insurance firm paid out for each claim

- inventory of customer’s home (photographs or videos uploaded by customer).

Do you have other ideas ?

I am sure there are other initiatives that insurance companies and insurance agencies / broker firms and their producers could pursue to make ‘invisible’ insurance visible to insurance customers.

What ideas do you have?