I’m not sure if this will help the many threads of whether Business Interruption (BI) should or should not be covered if the commercial P&C insurance policy excludes BI claims from being triggered by bacteria / viruses / pathogens but …

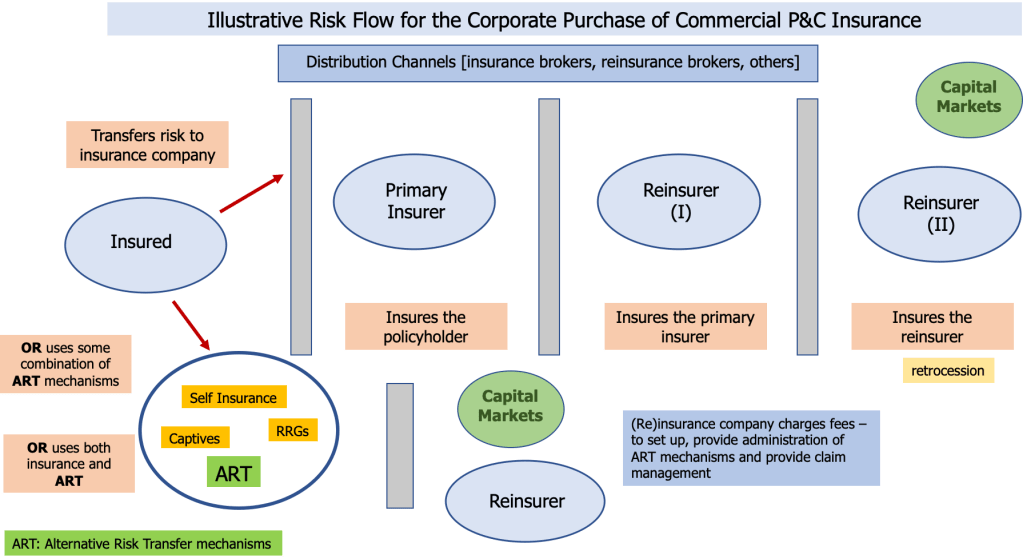

… I thought an illustrative visual diagram of a simplified risk flow capturing the key participants in the insurance transaction might help. I apologize for not including Excess & Surplus Brokers in the diagram.

This illustrative risk flow is for most of commercial P&C insurance purchases (that are accepted by the insurance firm). [RRGs means risk retention groups.]

Obviously, I don’t include the policy language / contract of any insurer selling policies that exclude BI coverage. I’ll leave that to those of you who can gather policies together and review them.