Do insurers need to keep up with the pace of technology change? How should insurers prepare to maintain (or exceed) the pace of technology?

I think we should consider some questions before providing any answers.

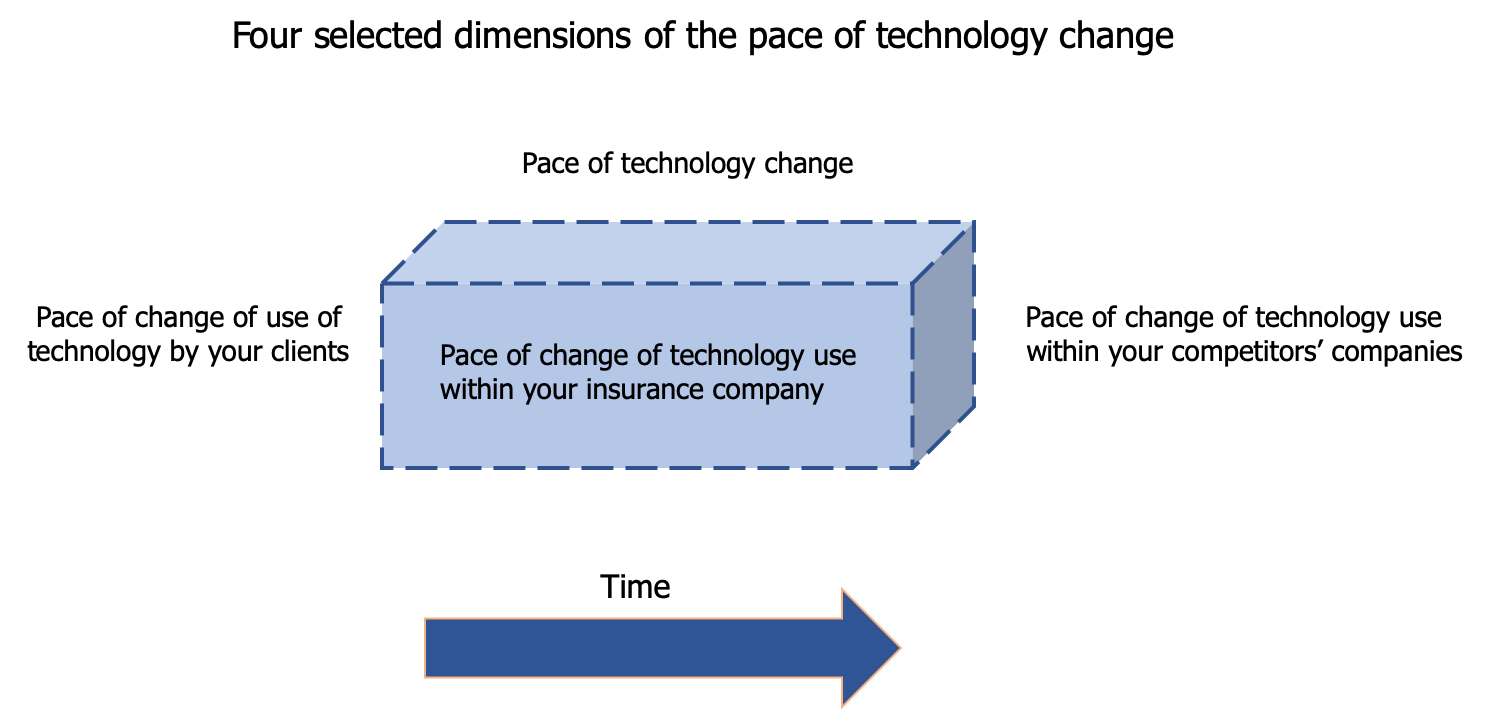

The illustration below captures four selected areas that the pace of technology changes impacts.

But before diving in, I have a premise to discuss augmented with some considerations …

My premise is that the pace of technology change of any of the selected four dimensions differs within your insurance company (and for the purposes of this post I am including the insurance broker/agency firms that your insurance company uses to go-to-market), within your competitors’ companies, and within your clients’ use of technology; within various lines of insurance; within the various Systems of Record, Systems of Engagement, Broker Management Systems, Systems of Insight, and Systems of Finance that your company uses; and across various geographies that your company conducts business.

To be more complete in our thinking, we should consider that the pace of technology change will differ within and across your entire chain (or value web, if you prefer) inclusive of each of the 3rd party contractors your firm uses to get and keep customers.

I include the 3rd party sources your company uses to gather information for underwriting purposes and 3rd party contractors your company might use for / directly after your client’s first notice of loss (whether for claim adjudication, fraud analysis, property remediation, physical rehabilitation, legal / lawsuit management, and eventual flow of funds from your company to any financial institutions to the claimant).

The ‘world is not flat!’ At least, the world of insurance is not flat!

Now turning to the diagram, it shows four selected dimensions of technology change that have different paces, including the pace of change of technology itself.

Herein lies another question (which I purposely blurred in the diagram): what are the changing pace of technologies and the changing pace of applications of technology in each of the four dimensions?

Before answering the question that I posed at the beginning of this post, I suggest we also take into consideration that there are three separate interrelated issues in play: the life-cycle of technology is one issue; the life-cycle of applications of each technology is a second issue, and the adoption of each application of each technology (also not shown in the diagram) is yet a third issue.

My answer to the question: yes, insurers need to keep up with the pace of change of technology. BUT, and isn’t there always a ‘but’, each insurance company must decide for itself what technology or technologies they need to maintain pace with, what applications of each technology they need to pilot and subsequently implement, and where in their value chain it makes the most sense to pilot and implement the applications (of each technology).

Insurers can see for themselves the downsides of not maintaining pace with the changes of technology. Usually, because the entire industry (pick your favorite major insurance line of business) is so slow to adopt new(er) technologies, the downside tends to be almost unmeasurable. The ‘needle is slow to move’ but it does move nevertheless.

Carpe Diem or Carpe Manana?

The decision rests entirely with each insurance company.

I believe change in the industry will come from within. It will happen by building parallel tracks to first generate new business and then serve to transfer legacy business. The key variable will be whether they build the parallel tracks on their own or partner. Do they have the DNA for change? Also this change may drive some industry consolidation

LikeLike