Insurance products currently do a lot of heavy lifting for insurance carriers. Insurers should expect products to do much more to strengthen competitive success.

Insurance products are meant to simultaneously attract customers and generate profitable premium flows throughout the product’s existence on the carrier’s books. Insurance products, taken as a complete portfolio, also represent a significant part of the carrier’s competitive face to the marketplace. Moreover, as importantly as the competitive presence, insurance products represent the risk appetite of an insurance carrier.

Insurers demonstrate changes in their risk appetite through elimination of existing products, alterations to existing products, and introduction of new products. Concomitant with new products and alterations to existing products, insurers also make their shifting risk appetite profile evident with changes to their pricing and underwriting practices.

But insurers should consider their set of products not just as an outcome of the company’s strategy to reflect a specific competitive presence and risk appetite but also as a dynamic vehicle that continually shapes the tactical initiatives and operational processes that attract, service, and keep customers and producers.

To accomplish achieving a dynamism of products that continually demands reshaping how the insurance carrier faces and serves its markets, insurers should consider using product level frameworks. The frameworks will guide the product development process and simultaneously identify a set of requisite enabling activities to be created and deployed for each level.

To insurers who remind me that insurance product development is a never-ending activity, I agree with you. But my point is that product development should be much more than creating another product for your producers to sell to your target markets. Your products should be an interactive portal into essential customer-enabling initiatives of your firm. Using a product level framework will help accomplish that.

As an example, I am using Dr. Philip Kotler’s “Five Product Levels” model framework. I’ll consider two perspectives of his product model: first a general perspective and second, an insurance perspective.

Kotler’s product model: general perspective

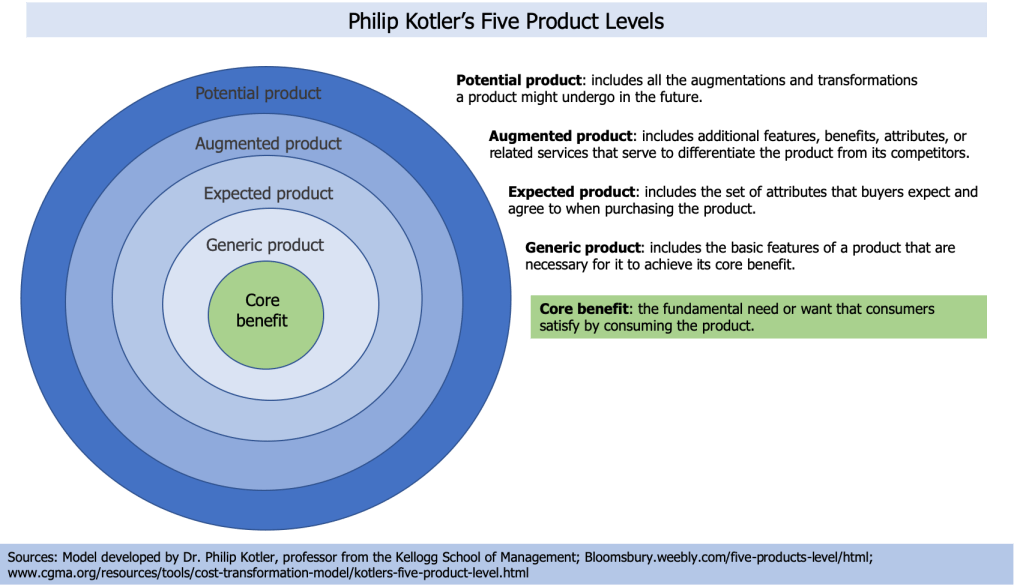

Dr. Philip Kotler is a professor in the Kellogg School of Management. During his career as a professor of management, Dr. Kotler created a model that delves into five major components of a product. (See visual below.) With no consideration of insurance products (until the next section), the five levels of his product level model are the:

- Core Benefit of a product: Satisfies the fundamental need of a customer buying the product.

- Generic Product: The basic features of a product to achieve the core benefit. (Technologists would call this the Minimum Viable Product – MVP.)

- Expected Product: The set of attributes that buyers expect when purchasing the product. I’d suggest that combining the Expected Product with the Generic Product could be called a Table Stakes product.

- Augmented Product: Characteristics the company augments the Table Stakes product (Generic plus Expected) to differentiate the product from its competitors.

- Potential Product: Augmentations and transformations a product might undergo in the future.

Each of the five levels can be ‘measured’ by the company creating the product or the customer or both. However, I believe that successful companies will consider the customer’s measurement as being more critically important than whatever the company (or its PR or MarCom staff) think.

Kotler’s product model: insurance perspective

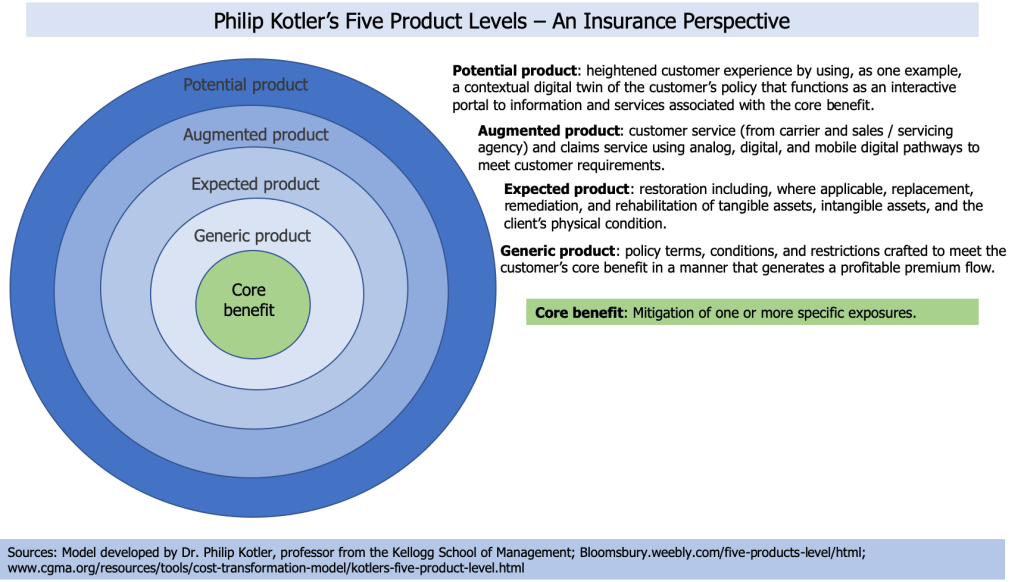

Keeping the general perspective in mind, I introduce an insurance perspective of Kotler’s product level model from a macro insurance perspective. (See visual below.)

Please keep in mind that I am not distinguishing between major insurance lines of business. However, the initiatives required to enable the accompanying initiatives of each product level will probably be different for each major insurance line of business. The product level initiatives will also differ for the lines of business under a major insurance line of business. I’m specifically thinking of product development for products within the short term disability (STD), long term disability (LTD), or long term care (LTC) lines of business that are sold by life insurers.

Re-perceiving Kotler’s model from an insurance viewpoint, my interpretation of the five levels are:

- Core Benefit of an insurance product: Mitigation of one or more exposures.

- Generic Insurance Product: Policy terms, conditions, and restrictions crafted to meet the customer’s Core Benefit in a manner that generates a profitable premium flow.

- Expected Insurance Product: Restoration from a loss including, where applicable, replacement, remediation, and rehabilitation of tangible assets, intangible assets, and/or the client’s physical condition.

- Augmented Insurance Product: Customer service (from carrier and sales/servicing agent/agency) and claims service using analog, digital, and mobile digital pathways to meet customer requirements. I include mobile apps within mobile digital pathways.

- Potential Insurance Product: Heightened customer experience (CX) by using, as one example, a contextual digital twin of the customer’s policy that functions as an interactive portal to information and services associated with the Core Benefit.

As with my discussion of the general perspective of the model in the section shown immediately above, I believe that combining the Generic and Expected Insurance Products are only Table Stakes for the insurance marketplace. Insurers need to determine how to exceed their current clients and target clients requirements when they purchase a Table Stakes product (in a manner that simultaneously generates profitable premium).

Point-in-time competitive advantage

Insurers wanting to strengthen their competitive position must develop initiatives for both the Augmented and Potential Insurance Products to stand apart from others in their target markets. Adding to the challenge of accomplishing this competitive activity is the fact that satisfying clients currently on the books and target clients will not necessarily be satisfied by the same Augmented and Potential Insurance Products.

Insurers must keep in mind that whatever initiatives they implement for either or both of the Augmented or Potential Insurance Products will provide a competitive advantage only for a point-in-time. Whether it is a shorter or longer point-in-time will depend on a variety of factors within the original insurance carrier’s value web (discussed in the next section) as well as the (to name only a few):

- insurance firm’s current customers’ adoption rate of new Augmented or Potential Insurance Products

- insurance firm’s target customers’ adoption rate of new Augmented or Potential Insurance Products

- agent/broker acceptance of the new Augmented or Potential Insurance Products (including any new training or licensing required to sell the new Augments or Potential Insurance Products)

- insurance firm’s competitor actions creating, marketing, and selling similar insurance products

- macro economic conditions.

An internal digital commerce platform

Creating an insurance product that encompasses all the levels discussed above – core benefit, generic, expected, augmented, and potential – requires significant continual communication and collaboration from many sources to identify, obtain, and/or create resources from the insurance carrier and its concomitant value web.

I’m thinking of an insurance carrier value web as including all of the insurer’s employees, producers, reinsurers, and third party contractors such as the contractors involved with rehabilitation and remediation of a client’s losses [that includes a life insurance beneficiary’s lost income stream] – in other words, the insurance carrier’s ecosystem.

One method of effectively, and hopefully efficiently, enabling the communication and collaboration flows and concomitant access, creation, and deployment of resources (inclusive of information and tactical initiatives and operational systems) is to use a digital commerce platform within the carrier’s value web (CVW Platform).

There may be some insurers who decide to enable access to the CVW platform to clients, particularly to large/jumbo commercial P&C insurance clients (e.g. CFOs, risk managers) or to large enterprise Employee Benefit insurance clients (i.e. CFOs, treasurers, benefit managers). For the purpose of this post, I assume that (authorized and secure) access and use (whether passive or interactive) of the CVW platform is only held to participants working entirely within the insurance value web.

(Personally I think that access to the CVW should be available to the large P&C, Life, or Employee Benefit enterprise clients. But this would probably be done in a second iteration of deploying the CVW Platform.)

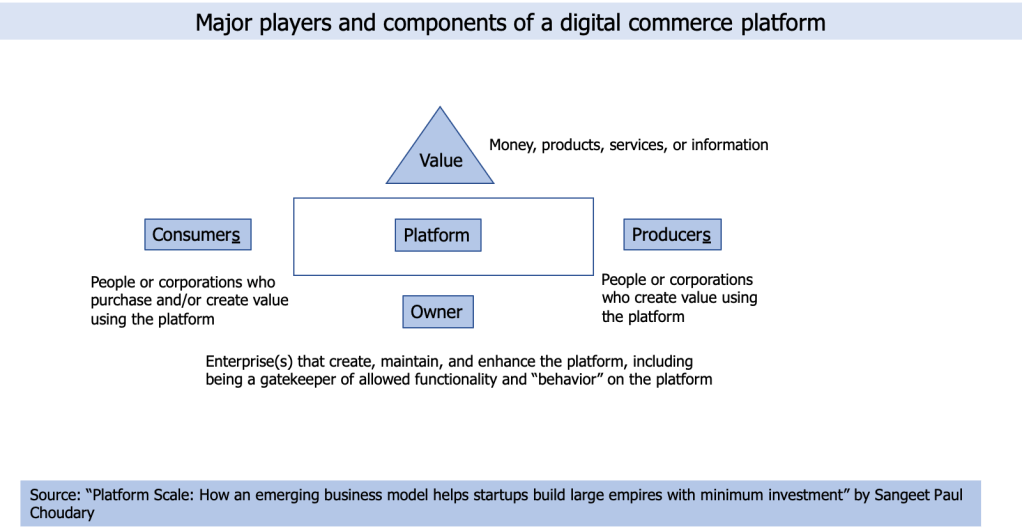

The concepts of digital commerce platforms have been cascading through the press, trade magazines, and, of course, technology sources for five plus years now. I show a visual of a digital commerce platform below from one of Sangeet Paul Choudary’s books on the subject.

Description and components of a digital commerce platform

What is a digital commerce platform? Mr. Choudary defines a digital commerce platform as: “a platform is a plug-and-play business model that allows multiple participants – producers and consumers – to connect to it, interact with each other, and create and exchange value.”

The key components are the platform itself, owner (or owners), consumers, producers (from a general perspective and not from our definition of ‘producers’ in the insurance industry), and value. I’ve written posts about digital commerce platforms previously (https://rabkinsopinions.com/2019/10/07/commerce-platforms-the-insurance-industry/) and plan to write another post on the subject in the future focusing on life insurers.

Components of an internal insurance digital commerce (CVW) platform

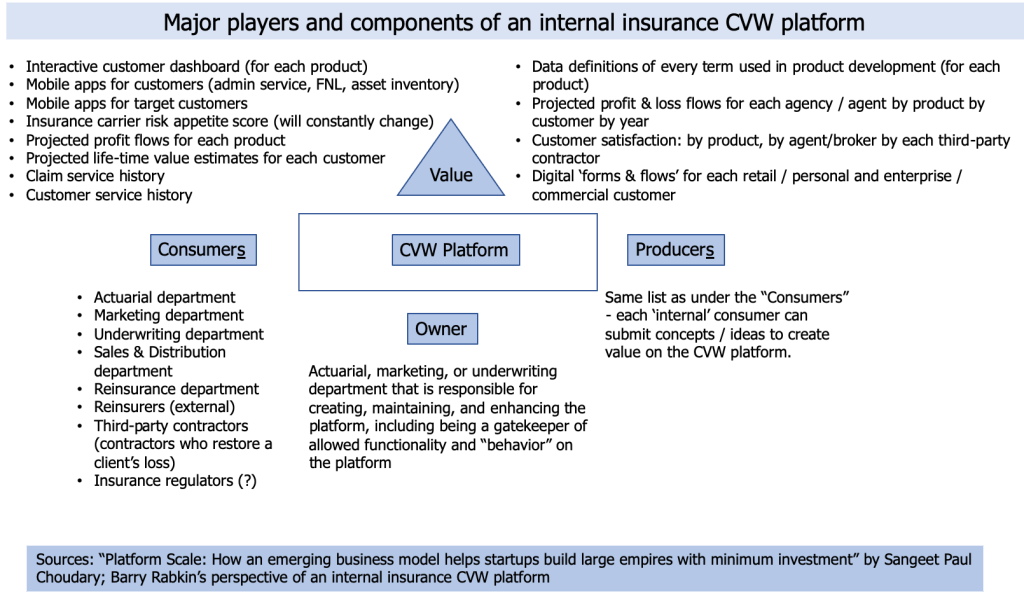

I believe that insurers should consider creating an internal insurance digital commerce platform. (See visual below for my ideas about platform ownership, producers, consumers, and potential value created for and to support product development for the five product levels. No, I didn’t attribute any specific ‘value’ to each of the five product levels.)

BTW I mistakenly omitted Legal, Regulatory (internal department), and PR (either internal or external) from the list of Consumers and Producers in the visual.

I’m attracted to the CVW platform’s ability to gather together multiple participants from different locations within the carrier’s headquarters, external field offices, and whatever locations around the world to simultaneously consume and produce value to enable product development generally and more specifically for each of the five product levels.

There are many challenges including:

- Who owns the platform: which department should “own” the CVW Platform. I have no problem with the insurer’s IT area actually building and maintaining it. But from what specifications? Personally I’d prefer the Marketing Department to own the platform but I could be swayed by arguments that the Actuarial or Underwriting Departments should own it. (I can hear the “yes, but who is going to pay us for our time and personnel” needed to create and maintain it?) I would be concerned if the Sales & Distribution Department owned the platform. First, salespeople want to sell not be bogged down in specifications and gate-keeping. Second, too many salespeople may be prone to let the platform guidelines be weakened to enable more sales (even if the sales generated future losses.)

- Requisite communication and collaboration capabilities: The insurer will need to provide the requisite communication and collaboration capabilities. I could foresee a veritable rabbit warren of communication and collaboration channels including email, IM, Salesforce Chatter / Slack / other ‘chat on steroids’ applications being used and/or favored by the different participants throughout the insurer’s value web.

- Security and privacy: The security and privacy of the data flowing into, created within, and flowing out of the platform to the various participants must be addressed and solved at the beginning of the project to create the platform.

- Convincing participants to join: Members from within the insurer’s value web will need to be invited and convinced why they should actually participate in the various activities required to make the internal insurance CVW platform a success.

Regarding the various tactical initiatives and operational considerations supporting each of the five product levels, I leave that to the insurer – and the platform owner – to determine how best to accomplish.

Concluding thoughts

Using a product framework extends product development to support and possibly reshape an insurance carrier’s strategic vision as well as to inform the tactical initiatives, and operational processes of an insurance carrier. The product framework and concomitant enabling initiatives reverberates through the decisions impacting resources, partnerships and alliances, and technologies (and their applications) an insurance carrier requires to financially succeed.

Extremely insightful and applicable in the fast growing e-commerce minded consumer marketplace. Look forward to your future post/report on Life insurers. Best

LikeLike