This blog post brought to you by insurance industry, investor, and entrepreneurial discussions of Netflix and Amazon.

There is, of course, one glaring difference between the products and services of the insurance industry and either of Netflix and Amazon: insurance is NOT a commodity. This remains true regardless of the insurance line of business we are discussing. That reality comes into play when thinking about and discussing all three entities: insurers, Netflix, and Amazon.

I thought it would help me to first discuss business models, moats, and insurance startups before writing a post comparing insurance firms to Netflix or Amazon. Readers of my posts (and comments on LinkedIn) must keep in mind that insurance startups are insurance firms and are NOT technology firms regardless of what technologies the insurance startups use or how “au courant” the technologies are that the insurance startups use.

I always define insurance startups from a ‘black-and-white’ legal perspective: if a firm MUST comply with insurance regulations then it is an insurance firm regardless of how old, current, or new the mix of technologies are that the insurance startup is using to get-and-keep customers.

In other words, no technology or technologies can EVER transform an insurance firm into a technology firm.

Let’s get to our discussion of business models, moats, and insurance startups.

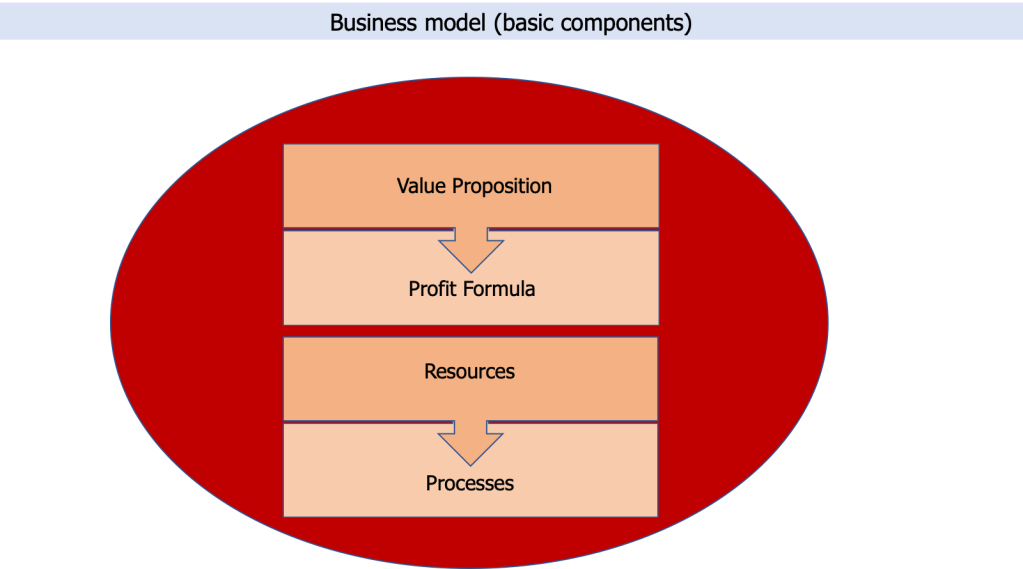

Business model (basic components)

There are many descriptions of business models available from a multitude of sources. I’ve created an illustration from an interview that Harvard Business Publishing had in late 2008 with Professor Clayton Christensen discussing “reinventing your business model”.

To paraphrase Professor Christensen’s description of a business model,

First, a firm creates a value proposition. The value proposition is defined in a manner to help someone accomplish a ‘job’ (i.e. fulfill a need) affordably, conveniently, and effectively. Next, the firm establishes a profit formula to deliver the value proposition in a profitable manner. Then, the firm identifies the resources it needs (i.e. buildings, equipment, people, products, and technology) to support the value proposition (and deliver it profitably). Finally, processes coalesce that are required to support the firm’s value proposition and resources simply and affordable.

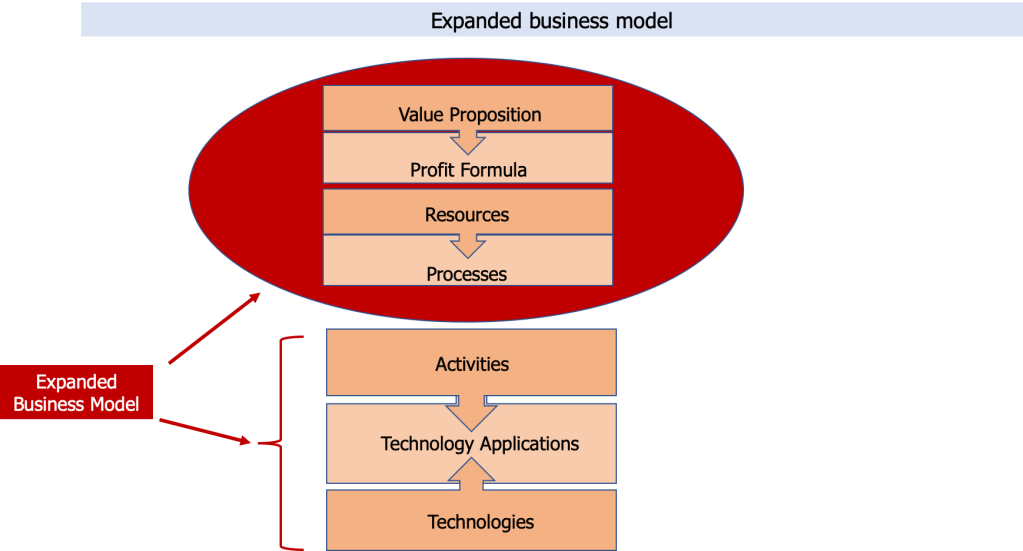

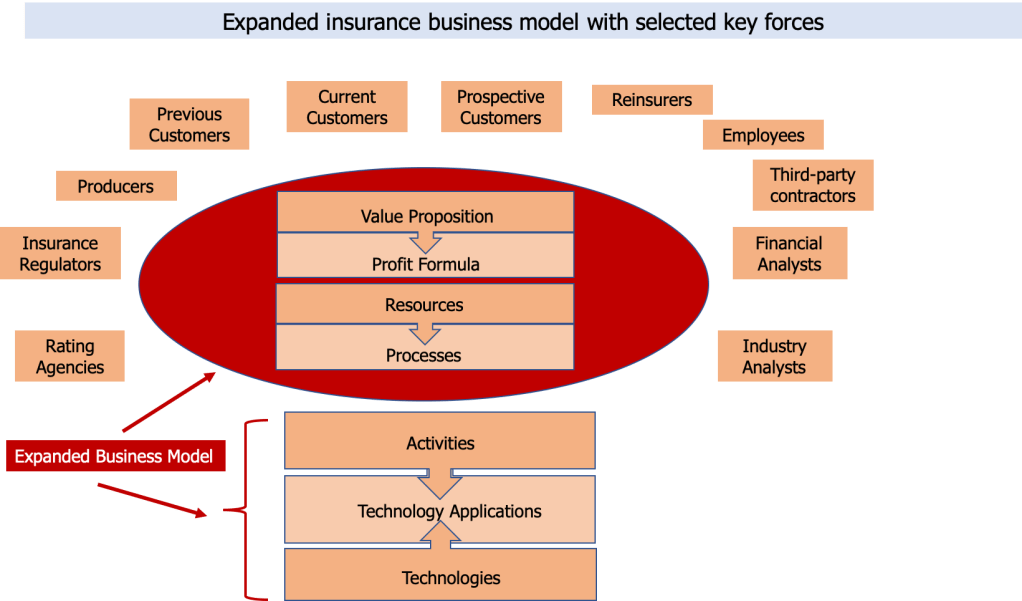

Expanded business model

For me, this is a reasonable and logical description of a business model before factoring in the forces within a specific industry that will alter the components to align with the realities of the specific industry. Later in this post, I discuss several selected forces of the insurance industry that shape (reshape?) the components.

However, I want to first expand on Professor Christensen’s business model components. My expansion (see visual below) encompasses three other major components: activities, technology applications, and technologies. Each of these are similar to Russian Nesting Dolls in that processes are comprised of several activities, each activity can be – and usually is – supported by several technology applications, and in turn, each technology application can be – and usually is – supported by several technologies.

Note that I take the term ‘technology’ to mean more than information technology or telecommunications technology. I suggest that P&C insurers when thinking about ‘technology’ consider the portfolio of materials technologies (inclusive of nano-technologies) and that L&A insurers consider the portfolio of ‘bio’ technologies inclusive of surgical technologies, bioengineering, genetic engineering, and cloning.

I think of my three additions to Professor Christensen’s description of a business model as an ‘expanded business model.’ Firms regardless of industry, whether startups or incumbents, need to consider how the set of expanded components enable the company to profitably deliver the value proposition (i.e. help a customer fulfill a need) affordably and simply to the company’s target markets. I don’t want to leave this unstated: “and with regard to the realities of the industry in question.”

Moats

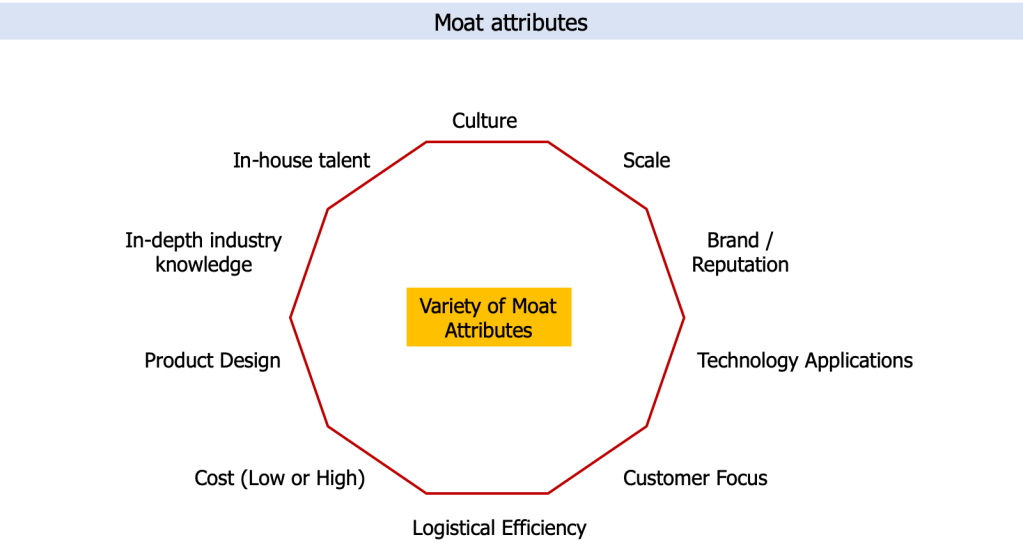

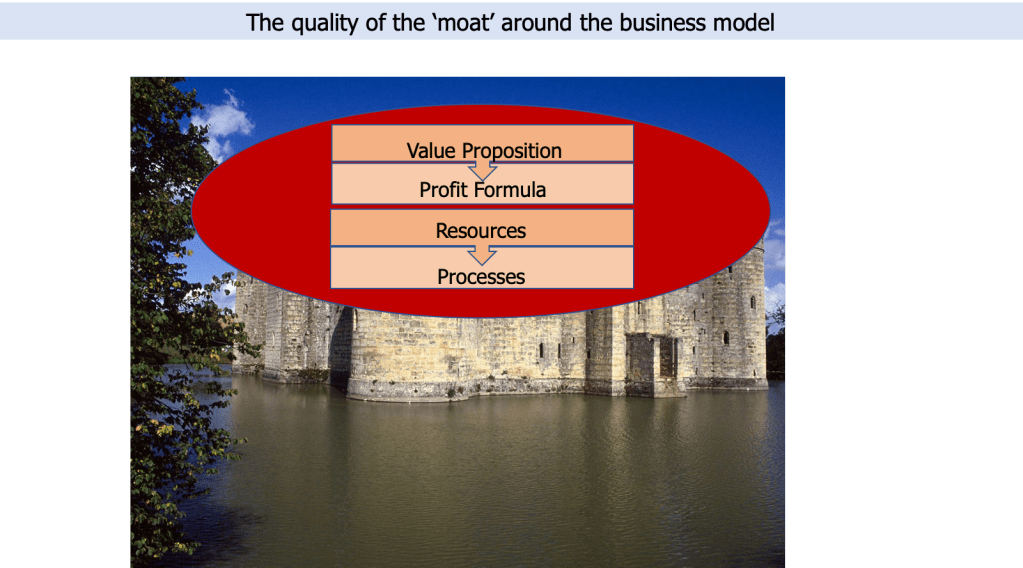

It is impossible to discuss business models without including a discussion of moats. The word ‘moat’ is used as a term to describe a firm’s (or actually, a firm’s business model) competitive advantage. Both startups and incumbents need a defensible moat.

It is very chic, very ‘terribly au courant’ to discuss moats, specifically for startups (and even more for insurance startups), as if the essence of a moat is entirely focused on the technology or technology applications a startup insurance firm uses to get-and-keep customers.

But there are more attributes beyond technology or technology application that can comprise a moat. The 10 attributes, inclusive of ‘technology applications that I have listed is only a partial list. (See visual below.) Please note that ‘Cost (Low or High)’ means only one OR the other for a specific product (or business unit). I realize that the same firm can employ both low cost and high cost depending on the product, solution, or market segment.

It is entirely possible – and I believe, desirable – for a firm to create a moat that is built on two or more attributes.

Moat mortality

“Guests, like fish, begin to smell after three days.” Benjamin Franklin

Regardless of which attribute or combination of attributes a firm uses to create their moat, a key question arises: what is the quality of the moat? That is, how fleeting is the defensibility of the moat? What might cause the moat to dry up? Will a firm’s moat last more than three days?

Moats will dry up. The attributes of a moat will age, wither, and die. The ‘mortality’ of a moat depends on a host of factors including, but certainly not limited to:

- emerging technologies and their applications

- changing customer needs, expectations, or demands

- staff reductions

- damage to the firm’s brand / reputation

- labor shortages

- changing economic policies (at local, state, or federal levels)

- external shocks (natural, man-made) to supply chains

- ? (you can fill in the ? here).

Regarding the first mortality factor (emerging technologies and their applications), we had an Arthur D. Little Center for Research and Development focused on banks, capital markets, and insurance when I worked there as an insurance management consultant in the Financial Services Practice. The Center’s objective was to provide clients with a ‘temporary’ window of competitive advantage through the use of technology.

We stressed to our clients that we were providing only a temporary competitive advantage because technology applications can be easily copied, newer applications based on the same technology emerge, or new applications from new technologies will arise quickly. To restate our position in the terms of this post: the mortality of a moat depending entirely or almost entirely on the applications of technology is extremely high.

Simply put: relying on technology (or a technology application) for a sustainable competitive advantage is a fool’s errand.

Expanded insurance business model with selected key forces

At this point, I’m finally turning ‘home’ to the insurance industry where I have spent my entire 40+ year career (with the exceptions of serving in the US Army, graduate school, and working as a ‘guest visitor’ at Bell Labs on the ‘Star Wars’ initiative).

Below, I illustrate an expanded insurance business model including selected key forces acting on an insurance company and its business model. This expanded insurance business model applies to both incumbent and startup insurance firms.

One way to consider an insurance business model (or a business model for firms in other industries) is that it sits in the middle of a communications web sending out and receiving signals from one or more of the forces shown in the visual. These forces act not just on the expanded insurance business model but also act on the insurance firm’s moat (whatever the depth the moat is at any given point in time).

Let’s get back to a point I mentioned earlier in this post that the realities of an industry will alter or reshape the components of a business model. That is certainly true for the insurance industry. Yes, insurers need to offer their products and services in a manner that is affordable and simple for customers. An insurance firm’s value proposition must help fulfill a customer need.

But, the insurance firms – incumbent or startup – must do so in a manner that comply with insurance regulators, offer products that are priced according to sound actuarial principles, and take into consideration that the industry’s product is a legal contract. That’s why Occam’s razor is not necessarily applicable to the insurance industry.

I’ve often described insurance as a risk management / mitigation service based on regulatory-accepted legal considerations surrounded by a financial wrap created to generate profit.

Quite the mouthful.

The reality is that insurers are in the business of paying claims but only those claims or the parts of a claim that meet the terms, conditions, and restrictions of the policy. That means that claims can’t always be paid immediately or even in any time frame that the most reasonable (non-insurance industry) person would consider as ‘real-time.’

Insurance fraud happens unfortunately far too often. Advances in technology including Deep Fakes will accelerate insurance fraud. [Note from Dec 7, 2023: that means that as society increasingly uses applications of AI Technologies, insurance claims could very well take longer to adjudicate.] To me, that means that lawyers, whether in-house or outside counsel, will always be critical players in the insurance industry. Similarly, I don’t see the Special Investigative Units (SIUs) disappearing as long as there are people willing to commit insurance fraud.

Insurance startups: a new species in the insurance ecosystem?

No.

Insurance startups are not a new species in the insurance ecosystem.

Insurance startups encompass new: insurance carriers, broking firms, managing general agencies (MGAs), and claim firms (to list only a few). These types of firms already exist in the insurance ecosystem.

The reality is that the essence of the value proposition must be the same for insurance startups as it is for incumbent insurers: mitigate or manage risk (for a specific set of exposures) in a profitable manner that complies with insurance regulations. Insurance startups, to be successful, have to find a way to offer their value proposition in a manner that incumbent insurers can not or don’t want to copy at all or in the near-term. BTW: Relying on investor funds to paper-over a startup’s losses or lack of profitability is a myopic – and dangerous – approach to bringing a new insurance firm to market. Eventually financial reality will drop as sharply as a guillotine’s blade.

(And if incumbent insurers don’t want to copy what one or more startups are doing, could it be that the incumbent insurers’ actuaries realize that offering the products or services that the startups are offering in the manner that they offer them will result in unacceptable losses, unacceptable levels of profitability, or no profitability at all?)

Giving credit where credit is due

To give credit where credit is due, I realize that insurance startups do use new(er) technology applications such as advanced analytics (i.e. forms of AI technology applications including algorithms / models, Big Data, cognitive computing, and/or machine learning). This use of technology applications does give the insurance startups a degree of time to capture customers. But let’s get real: the insurance startups have not reached into a parallel universe and pulled out technology applications that incumbent insurers can’t copy and also bring to market. There is no sustainable competitive advantage here.

To repeat myself, using technology (or technology applications) for a sustainable competitive advantage is a fool’s errand (however much money investors have plowed into the startup or however much enthusiasm the startup’s owners / management shout out to the world.)

Insurance startups have entered the insurance ecosystem by brokering Transportation Network Companies (TNC) insurance coverage, or insurance for telematics / usage-based insurance, or insurance for specific items in a person’s home for a specific time period.

Niches … all niches. I’ll agree that insurance startups creating their initial book-of-business on one or more niches is a clever idea. But niches do not a robust moat make. I can see the moat vaporizing now.

Important questions incumbent insurers should ask concerting insurance startups

Incumbent insurers fully realize there are many hundreds of startup insurance firms in-play or emerging around the world. There are quite a few ‘pump-and-dump’ conferences that are filled with enthusiastic investors and entrepreneurs bringing the startup insurance firms to the insurance marketplace. A seemingly never-ending waterfall of digital ink promoting the startups and simultaneously scolding the incumbents (for not partnering or acquiring the startups) continues to fill all variety of insurance media.

Nevertheless, incumbent insurers are partnering with (or acquiring) some of the startup insurance firms or wondering if they should partner with (or acquire one or more of) the startups. However, I recommend that before actually completing a (partnership or acquisition) transaction with an startup insurance firm, there are several important questions that incumbent insurers should consider asking the startup firm:

- What is the startup insurance firm’s business model?

- What best describes each part of their expanded business model?

- What is the level of money invested in the startup [and from what sources and what from what rounds of investment]?

- What is the number of customers that are on their books [not planned, not in the pipeline, not hoped for]?

- What exactly is the startup firm’s profit formula?

- What are the startup firm’s resources?

- What are the startup firm’s processes, activities within each process, technology applications supporting each activity, and technologies enabling each technology application?

- What parts of the insurance market, whether existing or niche or new (niche could equal new), is the startup striving to serve?

- What is the startup insurance firm’s moat?

- What one attribute, if there is only one, does the startup firm’s moat most depend?

- What is the mortality of the startup firm’s moat?

- Which moat attributes will dry up quicker than the other attributes?

- How, if at all, will that be a problem for the incumbent insurer?

- What parts of the incumbent’s business model will the startup’s business model:

- strengthen (by bringing in new customers in the same markets the incumbent already is in, for example)

- expand (by reaching new markets the incumbent is not in or does not plan to be for some time period?

- offer new products / services the incumbent is currently not providing?

- offer new technology applications, new skills / talent, new distribution channels that the incumbent is intrigued or interested in but has not yet decided to obtain themselves yet for whatever reasons?

- weaken and for what reasons?

- Whether partnering with the startup or acquiring the startup, what are the issues with integrating procedures, technology applications, staff, and culture between the incumbent and the startup?

- Is the investment (of money, people, skills, procedures, technology applications), whether in partnering with a startup or acquiring a startup, financially acceptable to the incumbent? If yes, at what time scale (immediately, short-term, or longer-term whatever these terms mean to the incumbent insurer) is the transaction acceptable to the incumbent?

Final comments

I’ve never shied away from my opinion that (99.99+% of the) insurance startups are born to be devoured by prey. Obviously, new insurance companies emerge in the insurance ecosystem but it takes a great deal of time. Insurance is not a commodity and that is a hurdle to succeeding in the insurance marketplace. Another hurdle is that insurance regulations exist for a very strong reason: insurance is all about helping people (and businesses) manage the risks to their lives, health, property, actions / behaviors, and income streams. Insurance is not a ‘game’ for corners to be cut because VCs and other investors want to rape and plunder the cash flow of insurance transactions.

For me, the startup insurance firms’ business models and/or moats cry out for extinction.

Barry, as always, a very insightful and carefully crafted article. I read it several times and even read by section from the bottom up. Yes, even comparing the lifespan of the sea turtles to that of incumbent Life insurance companies – give or take 150+ years. I believe two of the biggest weaknesses of current Life insurance business models are 1) customer service and 2) ability to change.

By service I am not referring exclusively to claim payments but to ability identify and meet all of the client needs during their life journey. They have tons of data to underwrite the client but yet they do not know the client. They do a poor job of identifying life events and their compensation model to their producers is highly skewed towards generating new sales. These misaligned objectives lead to poor customer service experience

On ability to change – to adapt insurance models to new consumer mindset and expectations requires a culture of change within the organization. So if focusing on acquiring start ups is part of the strategy concentrate on start ups that bring talented, experienced management team that knows how to orchestrate change. Poor change management skills destroy the value of acquired assets no matter how strong the moat is – it implodes from within the moat.

In the end, I agree insurance is not a commodity and its regulatory moat a high barrier for new entrants. So who wins when devoured by prey – a change agent. Message to incumbents avoid the “shiny thing syndrome” focus on the talent . To quote Nietzsche, “Those who have a ‘why’ to live, can bear with almost any ‘how’.”

LikeLike

[…] The following is from a post I wrote titled: Business Models, Moats, & Start-ups: An Insurance Analyst Perspective, (https://rabkinsopinions.com/2020/02/12/business-models-moats-start-ups-an-insurance-perspective/). […]

LikeLike

This was a fascinating deep dive into how business models and moats actually function in the insurance ecosystem. I particularly appreciate the point that startups, no matter how innovative their tech stack, are still insurance firms first and must play by regulatory and actuarial rules. The reminder that technology alone cannot sustain a moat feels especially timely. Your perspective on “moat mortality” is refreshing and realistic—far too many discussions overlook how quickly competitive advantages can erode.

LikeLike