This is the fourth of eight every-other-week blog posts excerpts from my book: “Stone Tablets to Satellites: The Continual Intimate but Awkward Relationship Between the Insurance Industry and Technology”. The publication date for this fourth post is April 20, 2022. The third blog post excerpted from my book was posted April 6, 2022. The last blog post of excerpted content will be June 15, 2022. Wells Media will publish the book on June 28, 2022 as a hard cover, paperback, ebook (Kindle), and audio book.

The excerpt of this 4th post is from the Insurance Commerce Section of the book. This section includes seven chapters which encompass a discussion of risk landscape perspectives; of customer perspectives; of carrier perspectives; of product development perspectives; of channel management perspectives; of producer productivity perspectives; and of claim management perspectives.

Let’s get to the excerpt ….

It is imperative that insurance carriers know what is happening on the risk landscape. By that I mean, understanding exposures that appear, are altered, or disappear from the risk landscape enables P&C insurers to make new or change existing coverage decisions.

As time progresses, many current risks become traditional risks and many emerging risks become current risks which, in turn, are destined to become traditional risks or disappear from the landscape entirely. This risk devolution from new to familiar means P&C insurers have several opportunities throughout the life-cycle of a risk (i.e. as the risk ‘devolves’ from emerging to current to traditional) to make decisions regarding whether to offer coverage for the risk and how to shape the terms, conditions, and restrictions of the offering for the risk.

(Note: I delve into more detail in the book about cyber risk and one of its variants – Deep Fakes – as well as the emerging Smart Homes environment with its plentiful opportunities for cyber risks.)

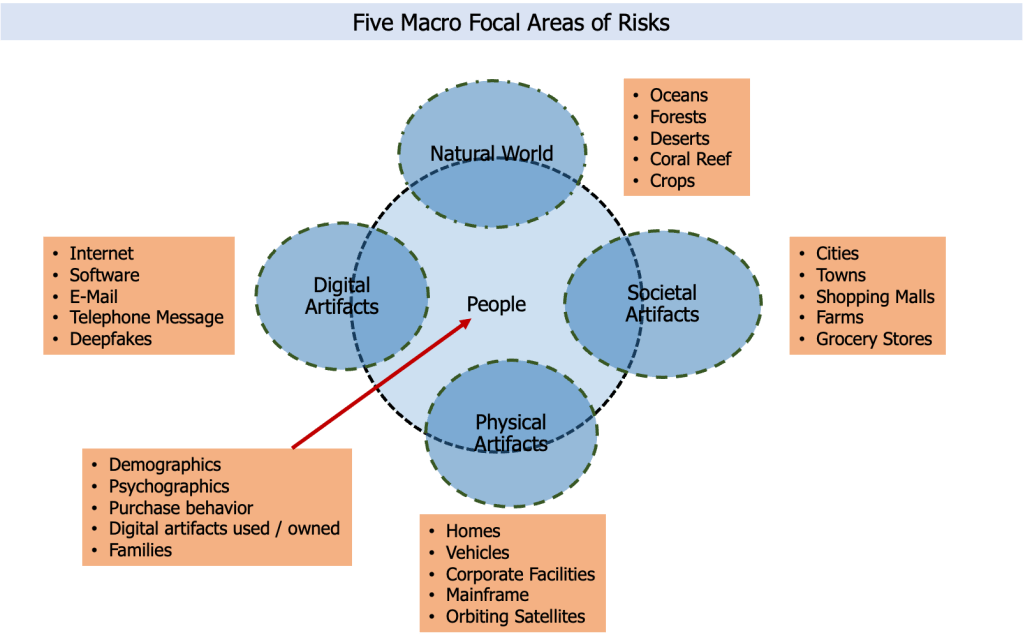

Macro focal risk areas

There are three key questions regarding how insurers could monitor the changing risk landscape:

- Where do risks originate?

- What forces drive the emergence of new risks?

- What forces drive alterations of existing risks?

I believe there are five macro areas that separately or in combination weave the changes to the risk landscape fabric: people, the natural world, societal artifacts, physical artifacts, and digital artifacts. Put another way, the fabric of the risk landscape continues to change through time as it is woven and rewoven by alterations in one or more of five major risk areas. (See visual.)

When considering the answers to one or more of the three questions, ‘People’ must always be included with any combination of the other four macro focal areas. That is because ‘People’ are not always involved with the creation of risks but are always impacted in some manner by any risks. It is ‘People’ who decide how to manage or mitigate the risks. For the purposes of monitoring the risk landscape, ’People’ can take one of many forms including, but certainly not limited to, consumers, family members, owners or employee of corporations and industries, home builders, farmers, educators, entertainers, healthcare provider, first responders, or delivery people.

Readers of the book will find that I also discuss data sources available which insurers can use to create a robust map of the risk landscape.

Answering the question: where do risks originate?

It is the interplay among and between the five macro focal risk areas, including the emergence and alteration of the attributes of each major focal risk area, that informs the reshaping of the landscape of risk.

———————

The next blog post will be published on May 4, 2022. I will excerpt content from one of the other chapters within the Insurance Commerce Section. Specifically, I will excerpt some content from the chapter titled Customer Perspectives. The last blog post of excerpted content will be published on June 15, 2022. The book will be published on June 28, 2022.