Understanding a problem

How do you come to understand a problem enough to resolve it effectively and efficiently?

More specifically, as an insurance professional, regardless of the functional area you work in, how do you come to understand a problem? How do you share your understanding of the problem with your colleagues? How do you and your colleagues collaborate about the problem and potential resolutions?

Two approaches come to mind: Insurance professionals review company or department documents and reports about the problem or ask colleagues who have past experience with it.

Taking a tools approach is also common: insurance professionals use one or more of several tools to:

- create and/or review tables of numbers

- create and/or review digital maps

- take and/or review photographs

- take and/or review videos.

Above approaches are necessary but not sufficient

The above approaches are necessary to understand a problem and potential resolutions. But they are not sufficient.

Why?

It’s not easy to share the results from the tools. It’s not easy to collaborate the results with geographically distributed colleagues (or even colleagues sitting in different locations of a large building complex). Yes, you can attach the results to emails or chats (or ask your nearby colleagues to gather around your computer screen and look at the results).

However with these tools to generate results, you’re just skimming the surface of the information that exists within the tables, maps, photographs, and videos.

Relating to the problem requires a ‘looking-glass’ moment

Resolving the problem requires you to relate to the information. The tools you use to resolve a problem should lead you to an ‘aha’ moment whether as a trigger to ask further questions of the information, request additional information, or present a resolution to the problem.

I suggest that to achieve that objective (getting to the aha moment by relating to the information), you need to immerse yourself – and your colleagues working with you to resolve the problem – within the information.

You need to move through the looking-glass, to borrow a concept from Lewis Carroll, to understand and interact with the information that underlies a potential solution.

Immersion technologies are a natural fit with the insurance industry

You need to use one or more immersion technologies.

Immersion technologies enable you to dive within the information. Immersion technologies and the insurance industry are a natural fit.

Similar to what should be an interlocking of geospatial solutions with insurance operations (such as marketing, distribution, and claims), immersion technologies should also be a primary go-to solution for many areas within the insurance value chain. And like geospatial solutions, immersion technologies offer insurance professionals a perspective that is otherwise unavailable.

Let’s discuss (at a high level):

- Immersion technologies

- Candidate value chain areas for immersion technology implementation

- Perspectives provided by immersion technologies

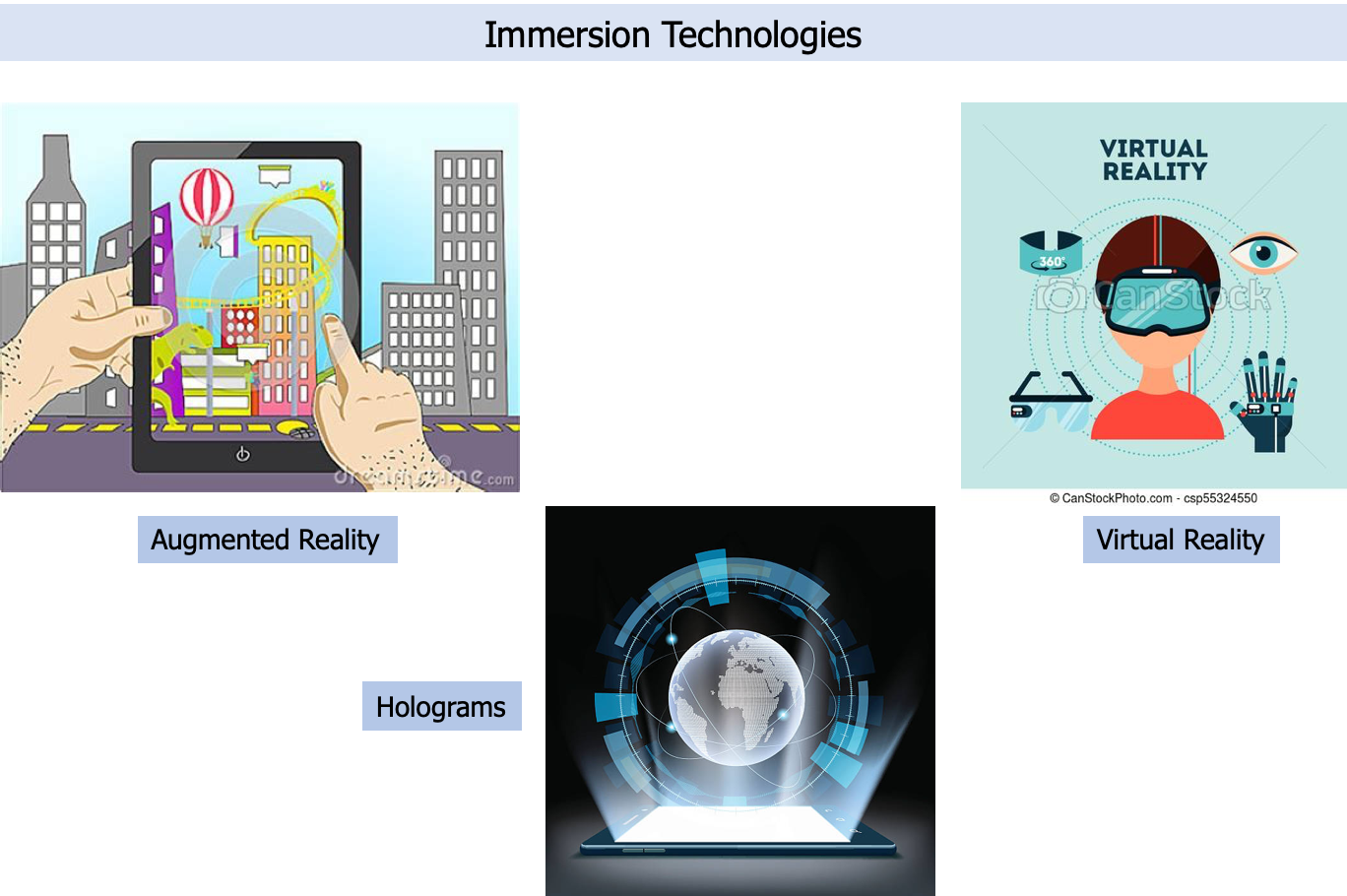

Immersion technologies

I believe there are three major immersion technologies: augmented reality, virtual reality, and holograms. I realize that ‘mixed reality’ also exists but for the purpose of this post I am going to exclude this type of reality (other than as an extension of augmented reality) and holograms (sorry Princess Leia).

Note: I do believe that holograms will have applicability for insurance applications including claim management, loss control, and underwriting.

The definitions/descriptions of augmented reality and virtual reality are (from Wikipedia):

- Augmented reality: Augmented Reality is an interactive experience of a real-world environment where the objects that reside in the real-world are enhanced by computer-generated perceptual information, sometimes across multiple sensory modalities, including visual, auditory, haptic, somatosensory, and olfactory. The overlaid sensory information can be constructive (i.e. additive to the natural environment), or destructive (i.e. masking of the natural environment). This experience is seamlessly interwoven with the physical world such that it is perceived as an immersive aspect of the real environment.

- Virtual reality: Virtual Reality (VR) is a simulated experience that can be similar to or completely different from the real world. Currently standard virtual reality systems use either virtual reality headsets or multi-projected environments to generate realistic images, sounds and other sensations that simulate a user’s physical presence in a virtual environment. A person using virtual reality equipment is able to look around the artificial world, move around in it, and interact with virtual features or items. The effect is commonly created by VR headsets consisting of a head-mounted display with a small screen in front of the eyes, but can also be created through specially designed rooms with multiple large screens. Virtual reality typically incorporates auditory and video feedback, but may also allow other types of sensory and force feedback through haptic technology.

Some take-away concepts from the Wikipedia descriptions of AR and VR for insurance readers of this post should be: immersive, seamless, and experience.

I’d also add ‘relate’ as a take-away although it is not explicitly stated in either description.

Experiencing VR myself first-hand

I’m not stating this ability of VR to help you relate to a problem as a conceptual or theoretical point. Some years ago in Cambridge, Massachusetts (maybe 10 or so years ago) one of my colleagues from Arthur D. Little set up an introduction for me with a VR startup.

My meeting with the new firm had two major components: discussing the applications they had brought to market and being given the equipment to wear (helmet, joy stick, haptic gloves) to experience Hurricane Andrew using VR gear. Truthfully, there was a third component of the meeting: the folks there telling me how they all put on VR gear and played multi-dimensional “Dungeons and Dragons” late Friday evenings to unwind. But let’s put that fun session aside.

First component: an application using their VR capabilities

They told me that one of the applications using VR were pharmaceutical scientists creating new drugs. They had modeled a set of molecules which the scientists could put their heads and hands into and around. The scientists ‘knew’ when the molecules successfully locked together from the haptic feedback in the VR gloves they used to push the molecules together.

Second component: putting the VR gear on me to view Hurricane Andrew

They put a helmet on me, gave me a joy stick and told me how to use it to ‘move’ at any degree of the 360 degrees, and gave me a pair of gloves with haptic feedback, and asked me to stand in a specific spot. They told me the model initially required me to stand hundreds of feet above a Florida neighborhood that Hurricane Andrew would hit.

With the VR equipment, I flew down to 10-20 feet above street level and saw the hurricane roll in and impact the neighborhood. (No, no-one threw water in my face so I could get the ‘full impact’ of the hurricane.) They restarted the model and I flew significantly higher to see the outline of the hurricane and its changing form as it flowed from the ocean into the neighborhood beneath my feet.

These and similar VR applications require significant computing power (this startup had a bank of super-computers), large amounts of data to be used for modeling, the skills needed to develop the models, and industry knowledge of the specifics being modeling.

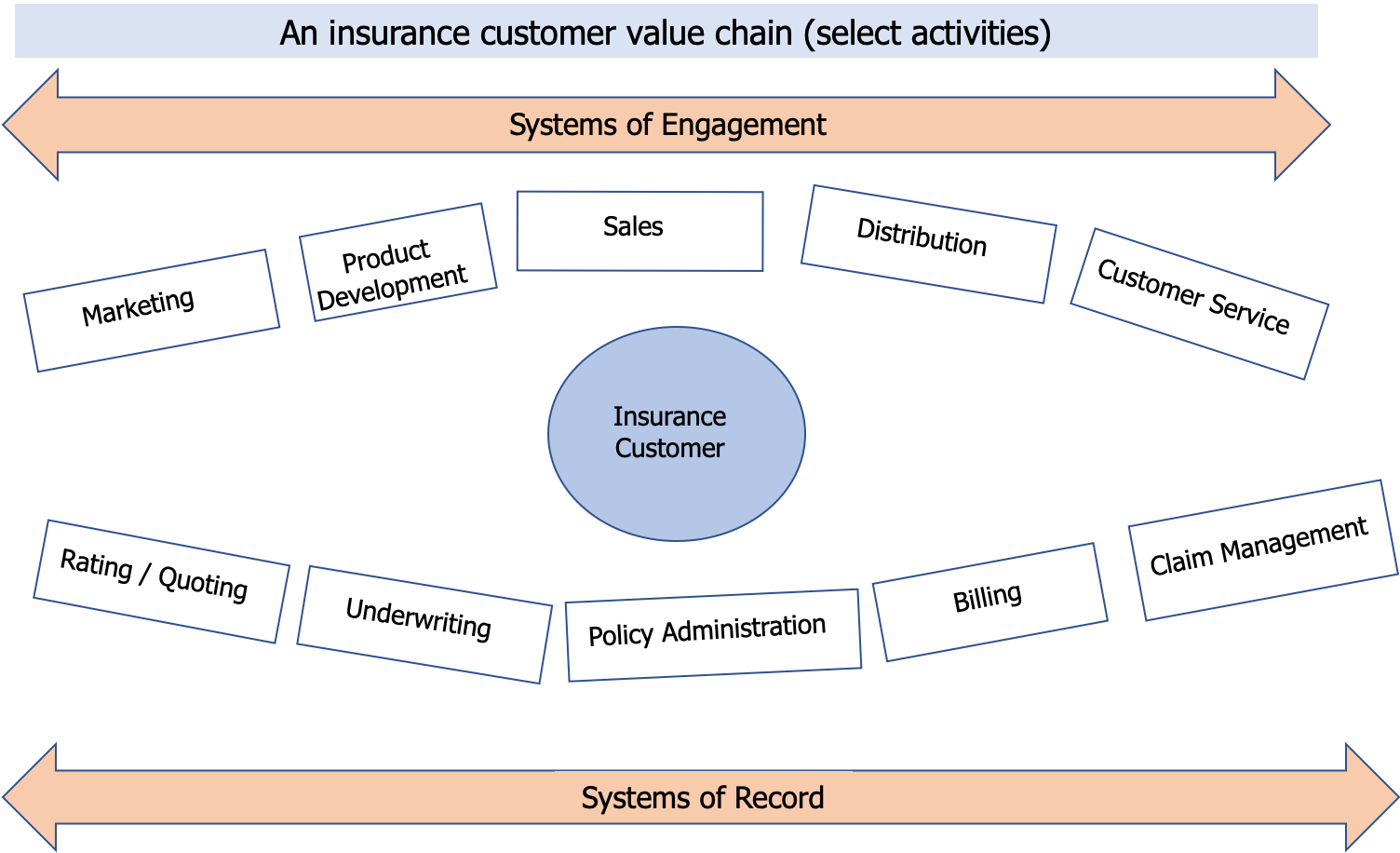

Candidate insurance customer value chain areas

The insurance Systems of Engagement (SoE) as well as claims management from the insurance Systems of Record (SoR) represent the obvious areas for either AR or VR applications. But if we give it a tad more thought, every activity in both the SoE and the SoR offer opportunities for either AR or VR applications. The main challenge for insurers will be to prioritize the potential AR or VR applications rather than brainstorming a list of opportunities.

BTW I think the claims management area serves in both the SoR and SoE value chains. We could also discuss why insurance agents / brokers serve as a bridge to transform the SoR activities into SoE activities for their clients. The ‘human touch’ is one reason the insurance industry is a world-class industry.

Using the illustration below, I suggest you identify a value chain area (or areas) as a drawing board to identify your own set of AR and VR applications. Don’t worry about (the many) resource constraints at this point. And don’t forget to think about applications that include vehicle body shops, property remediation contractors (including roofing contractors), construction firms, or new home / business communities being developed.

I discuss some VR and AR immersion technology application examples in the next section as a kick-start for your brainstorming exercises through the looking-glass.

Immersion technology perspective examples

The immersion technology perspective examples in this section encompass personal P&C insurance (PC), commercial P&C insurance (CPC), and life insurance (L).

I’ll leave it to you to put these visualizations into areas of the SoR or SoE value chains that you think are the best fit.

- VR: Visualization within homes or corporate facilities before they are actually build (layout, framing, wiring, plumbing, insulation, walls, appliances, energy use, type and cost of materials) (PC, CPC)

- VR: Visualization – topographical – of a planned community with roads, land/water features, and placement of homes, including ‘seeing’ through the walls of each home to see the quality and nature of the framing, wiring, plumbing, and wallboards. (PC, L)

- VR: Visualization of past and predicted routes and impact of hail storms (or wildfires or sinkholes) on homes and companies in a defined geographic area. (PC, CPC)

- AR: Visualization of a damaged home or company facilities (or vehicle) augmented with planned repairs (superimposing availability of cost of labor, type and cost of materials, and potential time-lapse photography to gauge total time of remediation). (PC, CPC)

- AR: Visualization of potential evacuation routes from a city shown augmented on a street level cityscape including existing buildings, land and water features, and existing vehicle and pedestrian traffic patterns. (PC, CPC, L)

Next steps

Insurers need to manage the AR or VR visualization as a medium that can be manipulated (including looking at the visualization from any of 360 degrees), commented on, collaborated with (whether on an asynchronous or synchronous basis), and shared with any number of colleagues regardless of where the colleagues are around the world.

I suggest that insurers:

- Fuse still pictures or video with AR

- Use existing IoT-enabled objects as ‘markers’ for AR or VR visualizations

- Identify where they could begin using either AR or VR for claims, underwriting, marketing, product development, or customer service

- Determine how to integrate the AR or VR visualization with one or more of their existing SoR and/or SoE.

It is up to each insurer to answer the question: “is it worth the computing power, the wearing of equipment, the time, the skilling of users (to understand how to use AR or VR visualizations and identify what they need to from the visualization, …

Are you already using AR or VR visualizations? Do you plan to use either AR or VR visualizations within the next 3-5 years?

Let me know.

Hi thanks for sharing thiis

LikeLike