I began my insurance career as a life insurance actuarial student. The key words are “began” and “student.” I enjoyed my time with John Hancock as an actuarial student before I was drafted into the Army. There were no deferments for actuarial students when I got my ‘Greetings and Salutations’ during that time period in The Vietnam War. (At that point, I decided to enlist in the Army rather than submit myself to the subsequent vagaries of being drafted.)

One force was definitely driven into me as an actuarial student: learning how to study and specifically ‘reading’ an actuarial textbook. That included concentrating on the front cover, the back cover, all the pages in between, all illustrations and their footnotes, and all the reference notes whether at the end of each chapter or the end of the book.

While I never got past the 2nd life insurance actuarial exam, I am positive that my brief experience as an actuarial student definitely helped me when I got my M.Sc. in Applied Mathematics when I left the Army.

Long way to state that life insurance was my first love of insurance. Thinking about and studying mortality curves, morbidity tables (yes, I was – and still am – a nerd), demographics / demographic cohorts, and life insurance client needs made for a pleasant experience. Years later, after the Army and graduate school, I went into insurance marketing / market research and many of my colleagues still thought of me as a ‘life insurance’ person.

But they were wrong because my re-entry into the insurance industry introduced me to every major line of insurance. I learned there was, indeed, life beyond life insurance. At the point in time when I semi-retired (August 2019), I’d say I’ve had more research and analysis experience with P&C insurance (both personal and commercial) in my career than life (or life and annuity). I’ve enjoyed learning about and seeing the differences of the market dynamics and competitive dynamics of each major line of business. I was in the health / employee benefits areas when I worked in the insurance industry which is one major reason I decided NOT to cover health when I became an industry analyst in 1997.

But two constants defined, or shaped, my insurance industry experience: 1) being customer-oriented (and by ‘customer’ I mean a person who pays the premiums for a policy – weird definition to the insurance sales and distribution folks, I realize) and 2) continually thinking, researching, and writing about the implications of geospatial capabilities on insurance commerce.

The following is a very long excerpt from a 2016 report I wrote about customer experience (CX), geospatial issues, and life insurance. Obviously, I allude to IoT and if I was to rewrite the report, IoT would play a larger role. Other than IoT, feel free to let me know what has changed since I wrote the report.

The need (mandate?) for life insurance value-add services

Traditionally, life insurance product development, marketing and sales are driven by customers’ current and future positions in the products’ life cycles. But most of these life insurance initiatives are neither focused on customers nor supported by geospatial capabilities. However, life insurers guided by the philosophy or equation “life cycle needs + location” are able to develop value-add services that, when augmented with life and/or annuity insurance, can better meet customers’ needs throughout the life cycle.

Geospatial capabilities have played a long supporting role in the insurance industry. Life and annuity insurers (L&A), in particular, have been using geographic information systems (GISs) at least since the 1970s to support marketing and sales.

However, at some point in the 1980s and continuing to the current day, insurers seem to have erroneously adopted the belief that GISs and other geospatial capabilities are primarily suited for property and casualty (P&C) insurance applications.

This post represents a “return to the future” because our initial involvement with GISs was almost entirely dedicated to creating and analyzing life insurance marketing initiatives to get and keep customers in the 1970s.

The medium is the message

GISs, or more accurately, geospatial solutions, represents a medium. Most of us have heard the expression that “the medium is the message.” Delving into the expression, Wikipediaexplains:

“…that the expression is a phrase coined by Marshall McLuhan. He meant that the form of a medium embeds itself in the message, creating a symbiotic relationship by which the medium influences how the message is perceived.

“Marshall McLuhan wrote in his book Understanding Mediathat ‘the personal and social consequences of any medium – that is, of any extension of ourselves – result from the scale that is introduced into our affairs by each extension of ourselves, or by any new technology.’

He later summarized his thoughts by stating the ‘message’ of any medium or technology is the change of scale or pace or pattern that it introduces into human affairs.”

What is the message for life insurers if a digital map is the medium?

If geospatial solutions are a medium, what is the message of the digital map for life insurers?

Before answering that question, we need to step back and appreciate that the medium of a digital map is a dynamic mixture of life insurance companies’ real-time and near real-time internal information about clients, selling and servicing producers, products, and marketing and sales campaigns, and external information about customers (i.e. social media data, use of the Internet of Things), prospects, and the geographic area itself.

With that realization as the context, we can now answer the question of what the message of the digital map is for life insurers: the ability to achieve visual geospatial coherence to provide a strong CX.

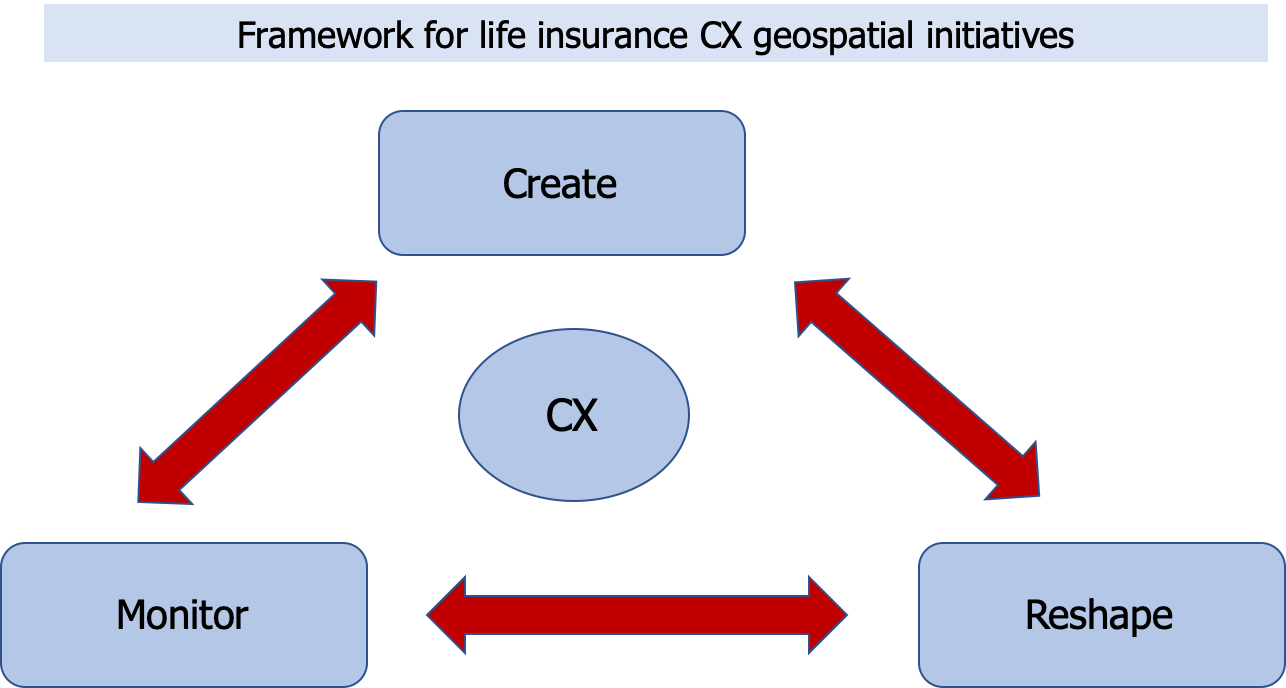

A CX-shaped geospatial framework

Life insurers should use a framework such as the one shown in the figure to build and strengthen their visual geospatial coherence.

In particular, life insurers should consider each of the three interdependent components in the framework as a repository of tactical initiatives such as:

- Create– Use geospatial solutions to create a new:

- Business model for the company by transforming the insurer into a “geospatial-first” insurance company. A geospatial-first insurer operates in the marketplace primarily through a lens of geospatial perspectives

- CX for either existing or new customers through the provision of value-add services not traditionally considered “insurance.”

- Reshape– Reshape existing products or activities, specifically:

- Existing life insurance products, by augmenting the client’s use of specific IP-enabled sensor-embedded objects into a service. The IoT objects could be home exercise equipment, sensor-equipped flooring, or “smart medicine bottles.”

- The value chain, by supporting the activities in each step of the chain through the addition of geospatial solutions.

- Monitor– Monitor CX-shaped geospatial life insurance initiatives, including:

- Data requirements and sources for geospatial current and planned initiatives.

- Frequency of use and training needs of people using geospatial initiatives including insurance company professionals throughout the value web (including field personnel and agents/brokers) as well as customers and prospects.

Geospatial life insurance client needs

Traditionally, life insurance product development, marketing and sales have been driven by customers’ current and future positions in the products’ life cycles. Life insurers create coverage for many steps throughout the life cycle to help customers manage the risk of dying too soon (i.e. not having sufficient income to protect beneficiaries) or living too long (i.e. outliving accumulated assets required to support income needs later in life).

However, life insurers that use the customer’s location to weave geospatial solutions into their product development initiatives, beyond supporting marketing and distribution, are able to take an important step to help their clients more than providing traditional L&A insurance.

Specifically, life insurers that are guided by the equation “life cycle needs + location” are best able to develop value-add services that meet customers’ needs during their lives.

Moreover, offering value-add services, whether bundled with a traditional life or annuity insurance product or not, provides life insurers with opportunities to:

- interact with their clients more frequently, which also implies that insurance customer service representatives will need to be trained in the full set of services that the company offers

- create a brand as a trusted insurance company (assuming there are no problems with the service or that the insurer creates partnerships with third-party providers to remediate any problems)

- generate non-risk-based revenue.

CX-shaped geospatial life insurance company initiatives

CX-shaped geospatial solutions enable L&A insurers to focus on specific customers or groups of customers more effectively by providing the coherent visual medium we discussed earlier in the report. Moreover, it is critically important that insurers use geospatial solutions to create services for clients progressing though different points of their life cycles.

Every person and business is located somewhere. This statement is obviously a tautology. Unfortunately, the very fact that every person and business is located somewhere has seemed to provide L&A insurers with a myopic perspective concerning how to use geospatial solutions.

But that doesn’t make this truism any less important to creating a robust range of CX-shaped insurance operational, go-to-market, customer service, and decision-making initiatives whether for traditional L&A insurance or for value-add customer services.

Note that when L&A insurers use CX-shaped geospatial solutions for any initiative, insurers must comply with all laws and regulations, including avoiding even a hint of redlining.